Communications Industry Forecast 2011-2020: Broadband Connections and Market Shares

Telcos and Cablecos Battle, But Wireless Broadband Becomes a Factor by 2020

For the first time this year, we’ve added broadband connections to our 10-year forecast…given that voice service is increasingly an “app” that rides the broadband network, we felt this was appropriate. What does get murky, however, is the definition of broadband.

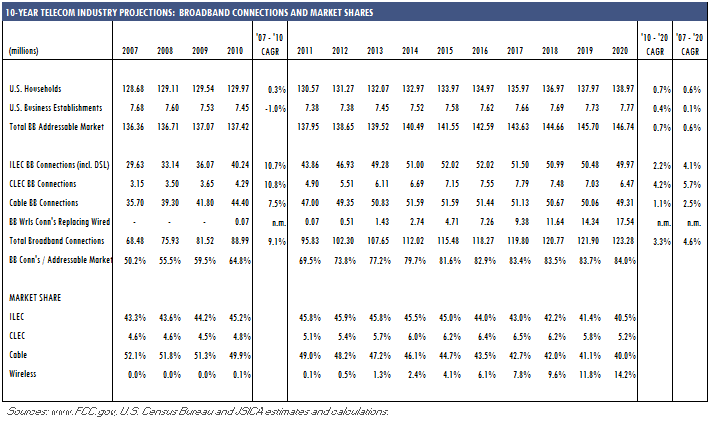

If you consider DSL connections, with average download speeds somewhere around 1.5 Mbps, to be broadband, then the telcos (ILECs and CLECs combined) are hanging pretty steady with the cable companies in terms of market share and connections. Using FCC reports, our own annual Phone Lines survey data, stats from the National Cable Television Association (NCTA) and public company information, we estimate that at the end of 2010 the ILECs had about 40.2m broadband connections; the CLECs, 4.3m, and the cable companies had 44.4m.

If, however, you define broadband as at least 4 Mbps (download speeds) as in the new Connect America Fund Order from the FCC, or as 3 Mbps as some prior FCC data reports have used, then the telcos would fall well behind in terms of broadband market share. Going forward we’ll no doubt need to evolve our thinking and estimates to these higher speed standards, but for the purpose of this year’s forecast, we are including all DSL connections.

Finally, we’ve included broadband wireless connections in our forecast. While the number of homes or businesses where a (for example) WiMax or LTE connection may have replaced a wired connection was very small at the end of 2010, we expect that increasingly broadband wireless solutions will lead to some level of broadband cord cutting.

First, in terms of the addressable market, we’ve combined the total number of households (including Puerto Rico and other territories) with the estimated number of business establishments nationwide (using Bureau of Labor Statistics data) to estimate the addressable market for broadband connections. From an estimated 137.4m addressable residences and business establishments at the end of 2010, we expect that figure to grow by about 0.7% annually, to 146.7m at the end of 2020.

Based on our estimate of 89m broadband connections at the end of last year, overall broadband penetration was just under 65% nationwide, up from 59.5% the year before. Looking out over the next ten years, we’re projected growth for both telco and cable broadband connections based largely on recent trends, but have also factored in overall penetration and the growing availability of broadband wireless solutions.

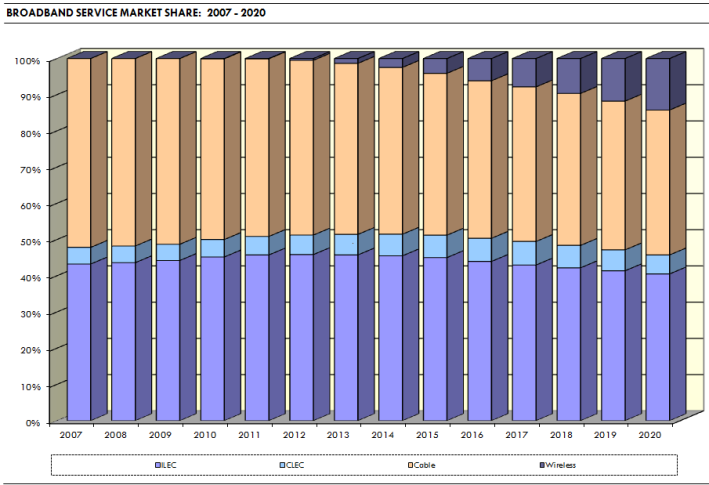

In the nearer term, ILECs and CLECs are expected to grow at a faster pace than cable or wireless due largely to their focus on small and mid-sized businesses, and also to the relatively strong growth being enjoyed by both AT&T (U-verse) and Verizon (Fios). By mid-decade, however, we think the wireless substitution factor and higher overall penetration forces wired broadband connections into a slow decline. Admittedly wireless isn’t a perfect solution for all broadband applications, but on the other hand, it’s likely to get better and it’s mobile. For lower end data users who aren’t streaming their video wirelessly, LTE and other wireless solutions are going to take their share.

By 2020 we believe overall broadband penetration nationwide will be 84% of the addressable market, with ILECs and CLECs controlling about 45%, cablecos controlling 40% and wireless providers grabbing just over 14%.

Richelle Elberg

Richelle Elberg

Reader Comments