Finally - Genachowski’s Big Announcement on USF/ICC Reform

Chairman Urges Americans to “Seize this Opportunity” for Universal Broadband

I can only imagine that hundreds, if not thousands, of rural telecom folks were eagerly (and nervously) sitting in front of their computers at 10:30 AM EST this morning in anticipation of FCC Chairman Julius Genachowski’s big announcement about USF/ICC reform. Unfortunately, the FCC’s live video feed left a lot to be desired. Genachowski did not divulge many precise details of the plan, which will be voted on by the Commission on October 27, but he gave a fairly thorough taste of the reforms. Earlier this week, he announced that the FCC’s plan would not be a “rubber stamp” of the price cap ILECs' ABC Plan, and it definitely does not sound like it is. There was really no mention of the RLEC Plan in today’s announcement (unless I missed it due to “technical problems” with the FCC live feed).

Genachowski opened by reiterating statements about the current USF/ICC system that have been said time and again since the National Broadband Plan was released: the current system is inefficient, wasteful, broken, unfair to consumers, creates competitive distortions that “companies have exploited in devious ways,” and causes uncertainty and legal disputes. Genachowski did give some credit to the old system at least, saying “It’s hard to imagine America being as successful without the telephone system,” which became ubiquitous due in part to the success of the current USF system. Well, we are living in a broadband world now, and the old system just won’t cut it.

Genachowski touted the benefits of broadband- job creation, private investment, emergency lifeline, a “connection to a world of knowledge” for students, and “a platform for entrepreneurs in rural America to start and grow small businesses.” He emphasized that broadband is a necessity, not a luxury, which is “not just a theory, it’s a fact;” and “the cost of digital exclusion [grows] higher every day.”

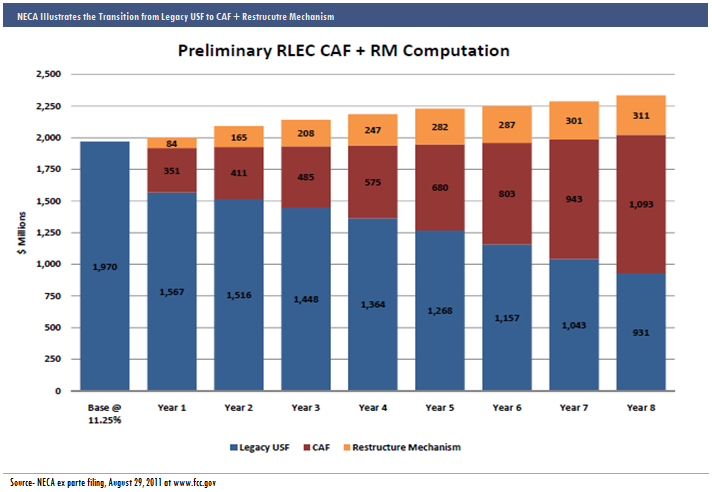

So what about the reforms? One of the key elements will be establishing the Connect America Fund to ensure universal broadband availability in unserved areas. The CAF will potentially help deliver broadband to 18m people in 5 years. There will be a Mobility Fund, but Genachowski did not say how much money would be dedicated specifically to mobility—I’m sure the rural wireless stakeholders are very curious about this. He did say that “the Mobility Fund will provide significant ongoing support for rural mobile broadband.”

CAF support will not replace private investment, and it will be targeted exclusively at areas without an unsubsidized competitor. CAF support will be distributed via “competitive processes,” which means reverse auctions, and it “will be conditioned upon complying with rigorous obligations to serve the public and meet the goals of universal service.” It sounds like the FCC wants to hit the ground running with reverse auctions in the first phase of CAF in 2012, but it was unclear on how the auctions would be structured or if (and when) they would apply to non-price-cap areas.

As for rate-of-return companies, Genachowski said that the plan will ensure “appropriate incentives to invest efficiently and receive predictable support.” No word on whether the rate of return would be reduced to 10%, but he did mention that there would be new accountability requirements and “benchmarks to ensure reimbursable expenditures are reasonable.”

The FCC appears to be taking a very hard line on ICC reform. The plan will supposedly reduce hidden subsidies paid by consumers, eliminate arbitrage opportunities, and “close loopholes” that allow phantom traffic and traffic pumping schemes. The “Recovery Mechanism” for lost access charges will be “tightly controlled,” and only some companies will be permitted to access these funds. Which companies, I wonder?

The role of states in the new CAF has been hotly debated in the last few weeks, with ABC Plan participants wanting to preempt states, and states wanting to maintain their role. Genachowski said that states will continue to have a “vital and meaningful role,” and COLR obligations will not be eliminated.

Genachowski concluded the announcement by insisting that “the plan will extend broadband to millions of Americans;” “spur private investment, create jobs and drive our nation’s competitiveness;” and create “massive consumer benefits.” He added that “every day without reforms is a day millions of Americans suffer increased harms…and millions of dollars are spent wastefully.”

I am anxiously awaiting the release of the draft rules to fill in the gaps on the issues that Genachowski did not explain very clearly. What did you think of Genachowski’s speech? Will RLECs get a good deal, or is it time to panic? Genachowski said, “companies that invest and manage their businesses prudently will have the support they need to continue extending broadband, and will be on a path to a more incentive-based framework in the future.” To me, this sounds like a stern warning for some, and a reassuring message to the companies who have been investing “prudently” all along.

A transcript of Genachowski’s speech is available here.

Cassandra Heyne

Cassandra Heyne