Communications Industry Forecast 2011 - 2020: Overall Wired Connections Trends

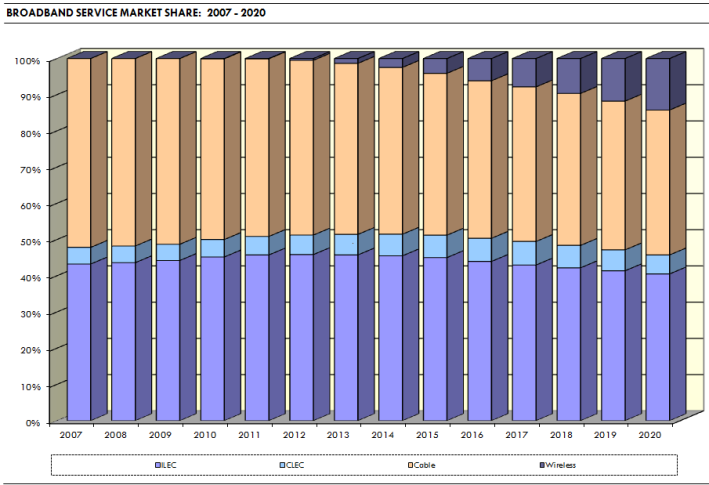

ILEC Broadband Penetration to Surpass 100% of Access Lines in 2015

For the past few weeks we’ve been sharing our Communications Industry Forecast for the coming decade—we’ve projected access line declines and growth in VoIP lines for both telcos and cable providers, we’ve forecast the proliferations of wireless devices and we’ve estimated total broadband connections through 2020. In this final installment in our series, I’ll consolidate and review the implications for ILECs and for cable companies in terms of overall connections trends and penetration levels.

(Note: We did not create a projection for video services or connections, which if included would dramatically change the total number of wired connections tallied here, given that cablecos are dominant in terms of video connections.)

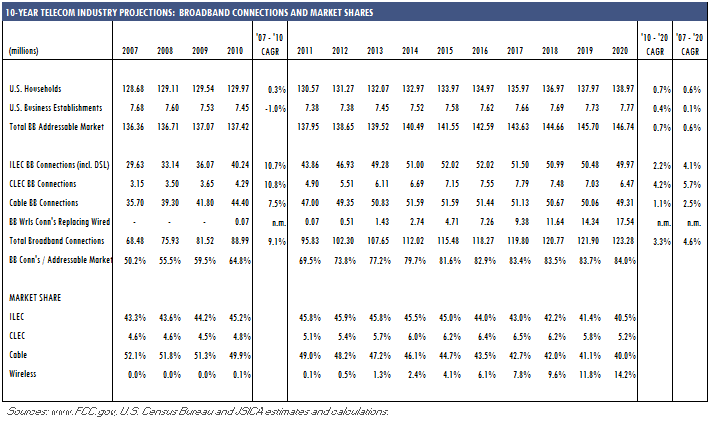

Based on voice and broadband connections only, we see the total number of ILEC connections falling at a 5%-5.5% pace over the next decade, as access lines fall at a 16%+ rate, VoIP connections increase at a 21%-22% rate and broadband connections grow slowly in the near-term before falling off somewhat in later years (due to displacement by broadband wireless service). Where we counted 144.75m telco access lines/VoIP lines/broadband connections at the end of 2010, we expect that toal to have fallen to just under 85m by the end of 2020.

By way of comparison, the cable companies total connections for voice and broadband service numbered just more than 70m at the end of 2020, but we believe that total will hold relatively steady over the next decade. Both VoIP and broadband connections are expected to increase for the next few years before wireless substitution begins to cut into both voice and broadband service from the cablecos.

Based on current trends in the market, we believe telco broadband penetration of access lines will be approaching 50% by the end of this year; a decade out we look at it in reverse: about one-third of broadband customers will continue to maintain an access line with their telco.

On the cable side, we estimate that 60% of broadband customers will also take a voice/VoIP service by the end of this year; by 2020 we expect that to have fallen to around 53%.

Richelle Elberg

Richelle Elberg