January – April 2011: USF NPRM, AT&T;/T-Mobile Merger Dominate Headlines

A Veritable "Spring Awakening" of Blockbuster Agendas

Looking back over the year, there were so many exciting telecom regulatory decisions, actions and mishaps that I just had to do a “2011: Regulatory Year in Review” series, in part to keep it light before the holidays and in part to help predict what might be on the “hot list” next year. 2011 kicked off with the FCC’s controversial late-December approval of the Net Neutrality rules still stinging for many telecom providers, and 2011 is ending on a similar controversial note with the Stop Online Piracy Act debate in Congress (which, ironically, is almost the direct antithesis of Net Neutrality). But in between these groundbreaking Internet policy and legislation bookends, there was definitely no shortage of drama in all areas of telecom regulation.

January 2011: The stage was set for the year-long flurry of merger, joint-venture and consolidation activity with the FCC’s Jan. 18 approval of the massive Comcast-NBC Universal deal. According to the FCC’s Memorandum Opinion and Order, “The proposed transaction would combine, in a single joint venture, the broadcast, cable programming, online content, movie studio, and other businesses of NBCU with some of Comcast’s cable programming and online content businesses.” For those of you who were a little uneasy about a vertical and horizontal (depending on who you talk to) merger of this magnitude, the FCC imposed a variety of conditions including the “voluntary commitment” that Comcast provide broadband for $9.95 to low income consumers—we’ll see this pop up again towards the end of the year. Commissioner Michael Copps dissented, claiming the merger “confers too much power in one company’s hands;” and “The potential for walled gardens, toll booths, content prioritization, access fees to reach end users, and a stake in the heart of independent content production is now very real.”

Also in January, Verizon and MetroPCS jumped the gun on Net Neutrality appeals… but they fired before locking in a target that could actually be appealed. Eager parties had to hold tight for 10 more months before the rules were finally published in the Federal Register. (The ILEC Advisor: Verizon Appeals FCC’s Net Neutrality Rules, MetroPCS Joins Verizon in Suing FCC Over Net Neutrality Rules)

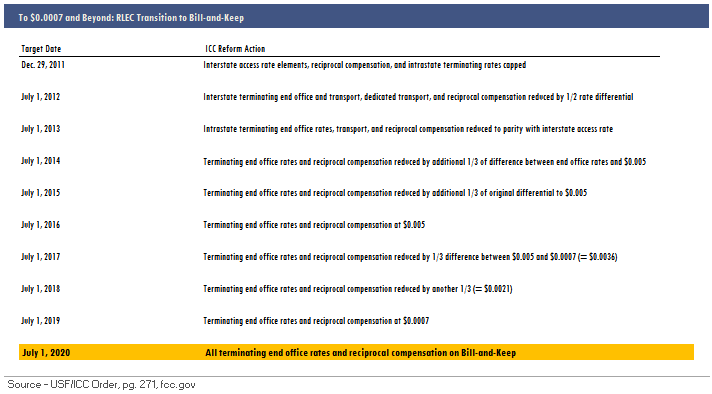

February 2011: I clearly recall at around this time last year expressing frustration (putting it nicely) that the USF/ICC Reform NPRM was pushed back when Net Neutrality took center stage. Well, we didn’t have to wait very long in 2011 for the 350-plus page NPRM that set in motion an entire year’s worth of anxiety and insomnia for the RLEC industry. Once the NPRM was released, the FCC pressed forward with the reforms at lightning speed (well, for the FCC anyway), and it almost seems surreal that we are now ending the year still trying to make sense of all changes to USF and ICC. Anyway, FCC Chairman Julius Genachowski demanded that USF/ICC reforms conform to four guiding principles: modernized to support broadband networks, fiscal accountability, accountability, and market-driven incentive-based policies. When the NPRM was revealed, Genachowski made sure to emphasis how the current USF/ICC system is fraught with waste, fraud and abuse; and he arguably made RLECs seem like Public Enemy #1. The FCC essentially insisted that the industry develop a consensus proposal in response to the NPRM, but as we will see, that didn’t work out so well… (The ILEC Advisor: Wireless Excess Highlights Needs for Universal Service Reform).

Not ten days later, we got another zinger- the NTIA’s National Broadband Map was released. RLECs scurried to check the data and make sure speeds and coverage were accurately portrayed in their service areas, only to find… A LOT of mistakes. My initial response to the map was “For $200m, why couldn’t they get it right?” JSICA’s Richelle Elberg wrote that the map was “disappointing, buggy, and the data incomplete;” and “it was a year in the making, it cost an awful lot of money, and it doesn’t seem to be fully baked just yet.” The biggest disappointment was that wireless providers like Verizon seemed to blanket extremely rural areas with 3-6 Mbps broadband, even though I know from experience in at least one such area that this is not an accurate representation—you see, it only takes one household in a census block to be served at that level for the entire block to be reported “served” on the map. Unfortunately, this is only one of the problems with the map, and nearly a year later it hasn’t improved much. (The ILEC Advisor: National Broadband Map Not All it’s Cracked Up to Be).

March 2011: Early in the year, there were a lot of rumors swirling that T-Mobile might be up for grabs—possibly by Sprint, which seemed like a long shot—would Sprint really want to repeat the technology incompatibility mess it had with its Nextel merger (The Deal Advisor: Sprint and T-Mobile in Talks (Again))? The telecom world shuddered on Sunday evening of March 20 when AT&T announced its intentions to abolish T-Mobile from the wireless market for a cool $39b—I was walking home from dinner and getting ready for the NTCA Legislative Conference when I got the news, and it is not an exaggeration to say that I nearly fell over. Anyway, there’s nothing like talks of ol’ Ma Bell reclaiming its monopoly to incite gut reactions from everyone—and I mean everyone. When the FCC comment cycle began, tens of thousands of consumers chimed in with very colorful opinions, one even likening the merger to rape (a comment that has literally haunted me all year…and don’t even get me started on the bizarre “interest groups” like the International Rice Festival who wrote in with questionable favor of the merger). Although many analysts initially assumed that the deal would fly through, JSICA was skeptical from the get-go, warning that the antitrust and FCC reviews would be harsh—and we were right. (The ILEC Advisor: AT&T to Acquire T-Mobile for $39b, Sprint Says it Will Vigorously Oppose AT&T Buy of T-Mobile, What’s Really Behind AT&T’s Acquisition of T-Mobile).

April 2011: USF/ICC Reform started heating up in April, with the first round of comments in response to the NPRM due on April 1 (ICC) and April 18 (USF), and two corresponding public FCC workshops held on April 6 and 27. On the ICC front, rural carriers were fairly unified in insisting that the FCC immediately adopt rules to curb arbitrage and classify VoIP as functionally equivalent to PSTN traffic. One highlight from the April 6 ICC workshop was when the panelist from AT&T (of course), asked sarcastically, “Does Iowa really need 200 small carriers?” The RLEC panelists expressed concern that ICC uncertainty contributes to low valuations for RLECs looking to sell or consolidate, which is contrary to the FCC hopes that the little guys will just consolidate once and for all.

The Rural Associations (NTCA, OPASTCO, WTA, NECA and state associations) released the RLEC Plan for USF/ICC reform, which many expected would be adopted by the FCC in the final rules—maybe not entirely, but at least in some capacity. The RLEC Plan focused on careful, “surgical” transitions for rural carriers to ensure reasonable cost recovery as well as continued broadband deployment, but without back-peddling the tremendous progress that rural carriers have made as a result of the original USF/ICC regime. Hundreds of other rural telecom stakeholders weighed in on the NPRM, many calling for Rate-of-Return stability, keeping the High-Cost Fund (now Connect America Fund) uncapped, and ensuring sufficient and predictable cost recovery. (The ILEC Advisor: Universal Service Reform – Their Two Cents: Nebraska Rural Independent Companies, Universal Service Reform – Their Two Cents: CoBank).

Finally, April also brought a sensible, well-received FCC Order on data roaming that “requires facilities-based providers of commercial mobile data services to offer data roaming arrangements to other such providers on commercially reasonable terms and conditions, subject to certain limitations.” Naturally, Verizon argued that the FCC overstepped its authority, but overall this Order signaled an important step forward for the FCC’s realization that voice and data are well on the road to becoming one and the same. Smaller rural wireless carriers applauded the decision, arguing that it will help reduce barriers to competition with the large wireless carriers. (The ILEC Advisor: FCC Adopts Order on Automatic Data Roaming).

As the mercury started rising in DC, so did the tension in the USF/ICC Reform proceeding. Stay tuned for more “2011: The Regulatory Year in Review” posts throughout the week!

Cassandra Heyne

Cassandra Heyne