Introducing ICC Reform: RM, ARC, and Eligible Recovery

FCC Drops Heavy Hints about its Preference for RLEC Consolidation (In Switching, at Least)

ICC reform: it’s perplexing, frustrating and complicated! If only that was all that needed to be said on this daunting topic…The FCC’s new rules for access revenue recovery are supposedly designed to “eliminate the uncertainty carriers face under the existing ICC system, allowing them to make investment decisions based on a full understanding of their revenues from ICC for the next several years.” Whether this desired outcome will ring true for RLECs, however, remains to be seen. For now, JSI Capital Advisors is here to help you try to understand the new rules (as we try to understand them ourselves).

Adding to the complexity, there are different rules for price cap and rate-of-return carriers—this article will only address rate-of-return carriers. Overall, it is important to add three new terms to your telecom vocabulary: Recovery Mechanism (RM), Access Recovery Charge (ARC), and Eligible Recovery. Understand what these terms mean, and how they will impact your companies, and you will be well on the way to understanding this bristly, convoluted web of changes we call ICC reform.

The Recovery Mechanism (RM) – Two Roads Lead to Access Recovery for ILECs

The RM is the overall framework “to facilitate incumbent LECs gradual transition away from ICC revenues.” In addition to reducing access rates to an end-state of $0 with bill-and-keep, the RM component of ICC reform gradually decreases the amount of access recovery that carriers may receive—and it sounds like the FCC eventually wants to eliminate the RM altogether. ILECs—but not CLECs—have two ways to mostly recover lost ICC revenues: by charging a limited fee to end-users (called the Access Recovery Charge, detailed below), and through CAF support (for RLECs, coming out of their $2b slice of the CAF pie). Note that CLECs can only recover access revenue by increasing end-user rates, which may create some challenges for RLECs with substantial CLEC operations.

The FCC argues that the RM will help eliminate uncertainty and allow ILECs “to make investment decisions based on a full understanding of their revenues from ICC for the next several years.” Driving the sweeping rule changes are some industry trends that both price cap and RoR carriers know all too well: declining demand for voice service and the related decline in minutes of use (MOU). Under the current system, access rates remain steady even though the market forces dictate otherwise. As a result, opportunities for arbitrage arise and incentives are distorted.

The FCC continues by arguing, “Ultimately, consumers bear the burden of the inefficiencies and misaligned incentives of the current ICC system, and they are the ultimate beneficiaries of ICC reform.” ICC reform is about benefiting consumers (even if rates are increased), not keeping carriers whole. The FCC does not think the entire RM burden should be placed on consumers, which is why the RM has two methods for recovery. What is confusing is that the FCC says consumers should not be responsible for the entire RM burden, yet both the ARC and CAF support come directly or indirectly from consumers. The ARC is a new independent end-user fee, and the CAF is collected through the traditional USF contributions methodology. Either way, consumers are paying.

In addition to consumer benefits like lower costs for long distance telephony and innovative new services, the FCC expects that carriers too will benefit from the RM framework: “Carriers will provide existing services more efficiently, make better pricing decisions for those services, and innovate more efficiently. Carriers’ incentives to engage in inefficient arbitrage will also be reduced, and carriers will face lower costs of metering, billing, recovery, and disputes related to intercarrier compensation.” This all sounds pretty great, but it definitely remains to be seen if RLECs and their rural customers will see any of these benefits.

Eligible Recovery – A 5% Annual “Haircut” and Pressure to Consolidate Switching

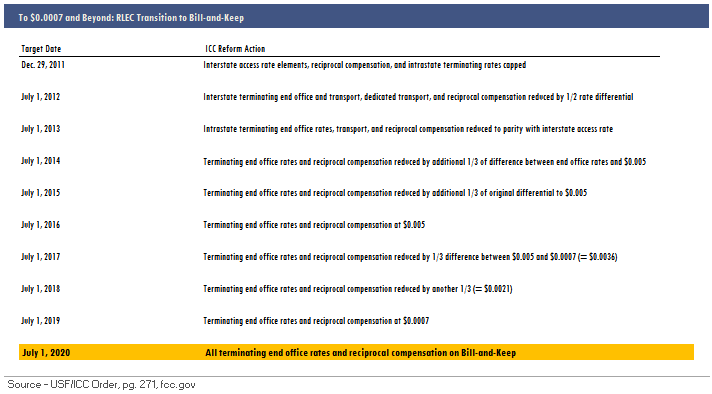

Determining Eligible Recovery is “the first step in [the] recovery mechanism.” The FCC contends that determining Eligible Recovery will help RLECs know with some certainty “their total ICC and recovery revenues for all transitioned rate elements, for each year of the transition.” The details for calculating Eligible Recovery are explained in the Order (starting on page 313), but essentially RoR carriers start with a “Rate-of-Return Baseline” equal to the carrier’s “2011 interstate switched access revenue requirement, plus FY2011 intrastate switched access revenues and FY2011 net reciprocal compensation revenues.” The baseline will be adjusted “to reflect trends in the status quo absent reform,” such as declining MOU and switching costs. The various access revenue components, illustrated below, have been projected to decline at different rates over the next six years, and the FCC has determined that an overall 5% decrease in baseline support for Eligible Recovery is “appropriately conservative.” The baseline amount is then recovered by three sources: traditional ICC revenue (which is decreasing in the move to bill-and-keep), the ARC, and the CAF.

It is important to discuss one seemingly passive-aggressive element of Eligible Recovery: the FCC’s apparent desire for RLECs to consolidate switching operations. On one hand, it might be entirely appropriate for some small carriers to share switches. On the other hand, this almost sounds like yet another situation where the FCC is dropping hints that RLECs should consolidate. One could get a feel that they are saying “consolidate switching today, merge tomorrow;” but this section of the Order is certainly open to interpretation. The FCC explains, “Our framework allows rate-of-return carriers to profit from reduced switching costs and increased productivity…For example, small carriers may be able to realize efficiencies through measures such as sharing switches, measures that preexisting regulations, such as the threshold for obtaining LSS, may have deterred.”

The FCC later takes a slightly harsher dig at RoR carriers: “Retaining rate-of-return regulation as historically employed by the Commission risks ‘perpetuat[ing the] isolated, ILEC-as-an-island operation,’ thus increasing the costs subject to recovery to the extent that, for example, each individual incumbent LEC purchases its own facilities, rather than sharing infrastructure with other carriers where efficient.” While it may be true that small carriers could realize efficiencies by sharing facilities, is it the FCC’s place to encourage sharing arrangements or should carriers come to this conclusion based on their unique market forces and cost structures?

Access Recovery Charge – “All End Users Should Contribute…”

The ARC, the direct end-user component of the new ICC recovery regime, is probably what consumers will be most interested in learning about. Some basic “rules of the road” for the six-year RoR ARC include:

- Residential ARC cannot increase by more than $0.50 per year, and cannot be increased further once a company hits the $30 per month Residential Rate Ceiling—this protects consumers in states with reformed rates, but provides very little wiggle-room for carriers who already charge close to, or above, $30 per month.

- Multi-line business ARC cannot be increased by more than $1.00 per year, and cannot be increased further once a company hits a $12.20 maximum per-line SLC plus ARC ceiling.

- The ARC revenue in one year cannot be greater than a carrier’s Eligible Recovery for that year.

- The ARC cannot be charged to Lifeline customers.

- ARCs must be allocated to a mix of business and residential customers, to “spread the recovery…among a broader set of customers, minimizing the increase experienced by any one customer.”

- Carriers do not have to charge the ARC; but if they don’t, the full amount that could be charged will be imputed from Eligible Recovery.

The FCC predicts “the average actual increase across all consumers to be approximately $0.10-$0.15 each year, peaking at approximately $0.50 to $0.90 after five or six years, and declining thereafter.” Carriers will need to study the costs vs. benefits of charging an ARC based on their unique competitive environment as well as the threat of reduced Eligible Recovery if the full ARC is not charged.

Still not Enough? Return to CAF.

If Eligible Recovery is not met though the mechanisms described above, carriers will have an opportunity to supplement their support from the CAF. The FCC “anticipates[s] that end user recovery alone will not provide the full recovery permitted by our mechanism for many incumbent LECs, particularly rate-of-return carriers.” Any supplemental CAF disbursements are subject to the same public interest obligations, like deploying 4/1 Mbps broadband upon reasonable request, as regular CAF support.

If this is still not enough, there is always the waiver process—however, carriers have to show serious financial harm and will be subject to a total company cost and earnings review. The FCC attempts to protect itself from carriers invoking the takings clause by insisting that the RM “goes beyond what might be strictly required by the constitutional takings principle underlying historical Communications regulations.” In other words—carriers should take what they get and be happy with it, because things could be worse. Keep in mind that all this ICC recovery is intended to be “truly temporary in nature.”

Well there you have it—ICC in all its anxiety-inducing glory! What do you think about these significant changes?

Cassandra Heyne

Cassandra Heyne