USF Reform - Their Two Cents: Hargray Telephone Company

Hargray Proposes Broadband Incentive Plan as an Alternative to FCC’s NPRM

On June 9 and 10, 2011, representatives of Hargray Telephone Company (“Hargray”) met with members of the FCC to discuss their alternative plan for USF Reform, the Broadband Incentive Plan (“BIP”). Hargray outlined the BIP in an ex parte filing and in reply comments filed on May 23 in the USF Reform proceeding. The BIP proposes to consolidate high-cost USF support and freeze per-line subsidies at 2011 levels, then tie future support to the number of telephone and broadband lines with a weighting factor based on broadband speeds. I find that this proposal is simple, forward-looking, and market-driven; and it does not discount the accomplishments that RLECs have made thus far in broadband deployment, nor does it leave traditional telephone subscribers in the dark.

Hargray’s ex parte filing describes how the BIP could provide a reasonable transition to a completely broadband-centric USF methodology. Support distributed under the BIP would be contingent upon the number of broadband and voice access lines per carrier, not how much money the carrier spends. According to Hargray, “due to declining trends in voice access lines, only those carriers that are aggressively building out infrastructure and delivering affordable broadband to their residents and businesses will be able to sustain levels of support at or near their current levels.” Hargray believes this will act as an incentive for RLECs to invest in broadband facilities and keep consumer prices low in order to stimulate demand and adoption. With per-line support frozen at 2011 levels, a carrier would lose support for each cord-cutter, but then have an opportunity to reclaim a slightly higher level of support for each new high-speed broadband customer.

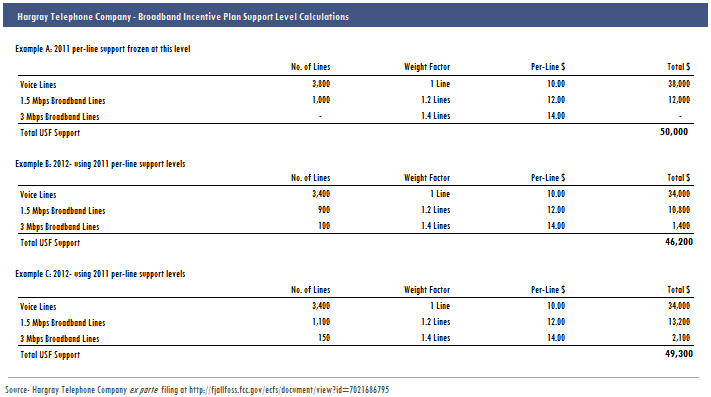

Hargray’s reply comments outline the possible benefits of the BIP: it could “promote broadband investment, economic stimulus and job growth;” “allow consumer choice to direct what services the fund supports;” and “manage the size and burden associated with the fund.” As for the mechanics of the BIP, Interstate Common Line Settlement support (ICLS), Interstate Access Support (IAS), High Cost Loop Support (HCLS), Local Switching Support (LSS) and Safety Net Additive support (SNA) would be combined, and per-line support would be frozen at 2011 levels. Each recipient of support would become a Carrier of Last Resort (COLR) in their study area. I believe the most interesting aspect of the BIP is the weighting factor for broadband lines. Hargray proposes that a broadband line between 768 kbps and 1.5 Mbps would receive support equal to one telephone line, but as speeds increase so would the support level. For example, broadband lines between 1.5 and 3 Mbps would be equal to 1.2 telephone lines, and broadband lines exceeding 25 Mbps would be equal to 2 telephone lines. The weighting factors could be easily adjusted in the future as the market dictates. Hargray illustrates how support administered under the BIP would reduce over time, assuming providers continue to lose landline customers. The following data was included in Hargray’s ex parte filing:

I believe the broadband speed weighting factor is an excellent alternative to the FCC’s proposed broadband support speed limit of 4 Mbps download, 1 Mbps upload (“4/1”). Although 4/1 may be a sufficient definition of broadband in the very near term, customer demands will rapidly outgrow this definition. I also think it would be very unfortunate if RLECs failed to upgrade broadband infrastructure because they could not receive support for speeds higher than 4/1, but the BIP may effectively solve this dilemma by encouraging RLECs to upgrade networks based on demand and likely customer take rates.

Another benefit of the BIP is that it will not undermine the still-relevant landline business in rural areas. According to Hargray, the BIP does not compromise the progress and investments that RLECs have made in both voice and broadband so far, and it “leverages the benefits provided by the existing [High Cost Support] program by establishing a mechanism that enables recipients to make additional investment in reliable and robust broadband services throughout America.” Instead of abruptly ending support for landlines, RLECs would continue to receive support based solely on the number of landline subscribers. As customers continue to migrate away from landlines, “the amount of support associated with voice-only services would drop over time consistent with the industry trend of declining voice lines.” Hargray proposes that BIP would act as a bridge to the Connect America Fund and potentially eliminate some of the risks associated with implementing a sweeping reform that could potentially leave RLECs without any USF support—or private investment opportunities. Hargray argues that the FCC “should adopt a structure that does not represent a risky start over.”

I agree with Hargray that the BIP might incentivize some RLECs who have been slow to invest in broadband infrastructure to finally step up their game. Although RLECs have traditionally been leaders in broadband deployment in rural areas, not every RLEC has modernized—this has been a significant source of criticism from the FCC and others, who claim that many rural providers are inefficiently utilizing USF. I think it is very unfortunate that the inefficiencies of a very small number of RLECs have been projected onto the collective RLEC community, and I think Hargray’s BIP could help overcome some of the negative sentiments about RLECs. Hargray shows their concern about this situation, and they argue that the BIP could “encourage companies to not only build broadband networks, but also to build them where customers want them and to price services on those networks so as to spur adoption.”

I applaud Hargray for submitting an alternative proposal because the FCC said from the very beginning of the USF Reform proceeding that they wanted to see solid models and data from the industry. I am particularly impressed with the BIP because it is forward-looking, practical, and logical. Hargray also argues that the BIP will reduce administrative burdens on the FCC, USAC and NECA because support would be based on estimated line counts rather than complex cost recovery calculations. I encourage RLECs to utilize the model illustrated above to calculate how much support they may receive in the future based on frozen 2011 per-line levels and a weighted broadband speed factor. Would your overall support decrease under the BIP, and would the BIP serve as an incentive to invest in broadband facilities capable of higher speeds?

Hargray Telephone Company is an RLEC serving Jasper and Beufort Counties in South Carolina with 41,000 telephone access lines and 16,400 broadband lines. Hargray’s reply comments are available here, and their ex parte filing is available here.

Cassandra Heyne

Cassandra Heyne