Large ILECs Lessening Reliance on Consumers

RLECs…Not So Much

Several of the publicly traded ILECs that we follow have made a concerted effort over the past few years to shift their customer base from residential consumers to enterprise customers and small/medium business customers. The rationale is clear—business users, regardless of the type of product or service they offer—have been considered less likely to cut the cord, or at least more willing to opt for a bundled plan that includes a wired voice offering along with broadband connectivity. Windstream (Nasdaq:WIN) has been a vocal proponent of this strategy and its desire to shift its revenue base from consumers to business was a clear factor in several of the acquisitions it made over the past two years.

We decided to take a look at the trends in business versus consumer lines for those public companies that report the breakdown. We then compared those trends with data we collect in our annual Phone Lines census, where we survey the nearly 1,200 LECs nationwide on their connections. Several hundred respondents each year provided information on the breakout between consumer and business lines.

What we find is that the largest LECs (i.e., RBOCs) have been reporting steady increases in the proportion of business lines in the mix. RLECs, on the other hand, have been reliant upon consumer lines for approximately 80% of their lines since 2003, with no notable shift in the breakout between consumer lines and business lines.

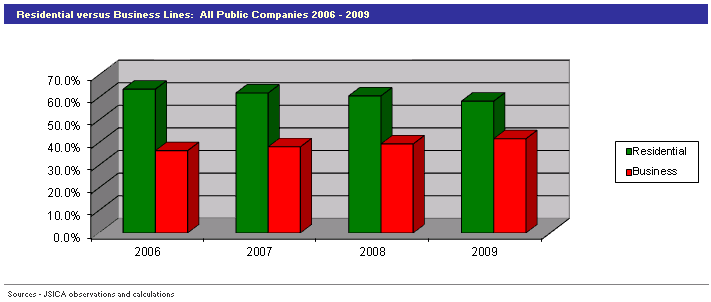

First the public companies. We found that 10 of the public ILECs reported a breakdown for business versus residential lines for at least some of the years between 2006 and 2009. And where in 2006 the percentage of business lines was about 36%, by the end of 2009 that percentage had grown to nearly 42%. These figures are, of course, heavily weighted by the two RBOCs—Verizon (NYSE:VZ) and Qwest (NYSE:Q)—that report the breakdown.

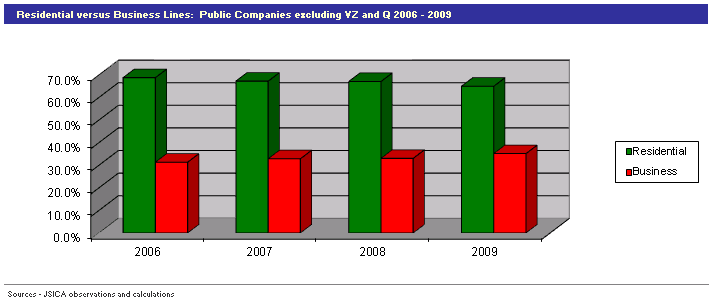

Next we had a look at the public companies excluding the RBOCs. The eight remaining public companies reported that business lines accounted for 31% of total lines in 2006; by 2009 that figure had grown to 35%.

Of course, the larger LECs, and the RBOCs in particular, have suffered the steepest overall access line declines in recent years. If you assume that a large proportion of cord cutters are (were!) residential customers, than the shift makes sense. Most RLECs on the other hand, have lost lines at a rate of just 3% - 5% on average for the past several years.

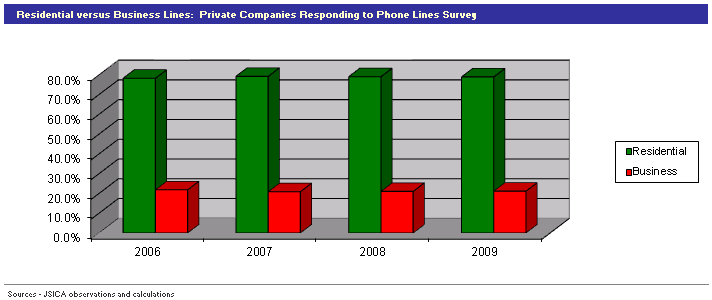

Based on data gathered in our annual Phone Lines census, where we survey each of the nearly 1,200 RLECs nationwide on their connections, we were able to find nearly 300 companies that had provided the business versus residential breakout for at least two of the years examined. And while the number and composition of companies included in the analysis varied from year to year, the proportion of business to residential lines was uncannily stable, going all the way back to 2003.

In 2003 our analysis indicated that nearly 80% of the access lines served by RLECs were for residences and just more than 20% were identified as business lines. Fast forward to 2009 and we find that 79% of lines were for residences and 21% served businesses.

So what does it all mean? Obviously, change comes more slowly to rural markets, and particularly in areas where wireless coverage may have been sub-par, mobile substitution has not occurred as rapidly. On the other hand, in those places where coverage is solid, or attractive VoIP options have been available, small business owners looking to save money may have made the switch at roughly the same pace as consumers.

Looking ahead, however, we wonder if there isn’t more that rural LECs can do to build up their importance to local businesses. Getting there first with a VoIP option may be a solid strategy, particularly if the local cable company is aggressively promoting the service. Fixed wireless solutions with a VoIP component may also work well in some areas, especially for those who’ve warehoused spectrum over the past decade. At the end of the day, both consumers and business customers will be seeking the best value for their dollars, but a healthy relationship with local business owners could well be one of the best defenses an RLEC can employ.

Richelle Elberg

Richelle Elberg