Subscribers Are Paying Hefty Interest on the Handset “Loan”

In Part 1 of this series, I described how Verizon Wireless (NYSE:VZ, “VzW”) and AT&T Mobility (NYSE:T, “AT&T”) are acting as unregulated market makers within the handset market, because of their overwhelming dominance, market share and resulting sway with equipment vendors.

Part 2 showed the calculation of the net present values of a hypothetical AT&T subscriber and a hypothetical VzW subscriber, under a scenario where the subscriber accepts a handset subsidy in exchange for signing a contract and alternatively, where the subscriber pays the advertised retail price. Not surprisingly, the NPV of each subscriber is sharply higher under the unsubsidized scenario than under the subsidized scenario; the difference between the two scenarios is supposedly explained by the out-of-pocket expense that wireless carriers incur to offer the discounted device to their customers. It is also used to rationalize the Early Termination Fee (ETF) that subscribers incur if they terminate service before fulfilling their contract. Now I will explain why I think this system is unfair to the consumer.

The following is a hypothetical situation that is faced by U.S. consumers every day. Consumer X arrives at the local ValueZone Wireless store to buy the new CoolPhone, which is manufactured by Apricot Electronics Company; the full retail price is $499.99 and the contract price is 199.99, implying a total subsidy of $300.00.

The consumer doesn’t like the idea of signing a contract and he takes issue with the fact that the implied subsidy is less than the ETF, which is $350.00. When the consumer points out this inconsistency (the ETF is greater than the subsidy), he is told that there is an additional discount available in the amount of $100.00, making the contract price $99.99. This brings the implied subsidy to a total of $400.00—this is beginning to look like a good deal. Still being uncomfortable with notion of signing a contract, the consumer asks if the additional discount can be applied to the full retail price. The answer is no, the additional discount is only applicable to the contract price and in order to get the additional discount, Consumer X must signup online.

Now things have become more confusing. There are three prices instead of two and two different implied levels of subsidy: there is the full retail price of $499.99, the contract price which is $199.99, implying a subsidy of $300.00 and the online contract price of $99.99, which implies a $400.00 subsidy.

But what if the real price paid to Apricot Electronics was really $100.00 less than the full retail price and that ValueZone Wireless had chosen to only pass those savings on to consumers who purchase the CoolPhone at the online contract price? For the consumer willing to forego the additional discount, the implied subsidy is $300.00 and the actual cash subsidy is $200.00. A similar situation hold true for the subscriber who signed up on line; the implied subsidy is $400.00 but the actual cash subsidy was really $300.00. Does this really happen? The answer is that I don’t know; none of the information that is needed to answer this question is ever disclosed.

The next issue that must be tackled is the interaction between the implied cash subsidy, the actual cash subsidy, the initial ETF and the ETF amortization. This task is difficult because the information provided in the subscriber contract, while seemingly simple, is in truth very confusing. Nevertheless, if we begin with the assumption that the inclusion of the ETF in the subscriber contract is a fair proposition, that the wireless carrier incurs an out-of-pocket expense at the time the wireless devices is sold and should be allowed to recoup that expense if the subscriber terminates the contract early, then we can proceed.

But what is the proper amount that should be paid for early termination? This is where the issue becomes murky and determining the amount is made particularly difficult because the actual amount of the cash subsidy is an unknown quantity.

The ETF policies for AT&T and VzW as it relates to smartphones are the following: AT&T sets the initial ETF at $325.00, for each full month during which the subscriber remains active on AT&T’s service, the ETF is reduced by $10.00. VzW, starts its ETF at $350.00 and, like AT&T, for each full month of service the ETF is reduced by $10.00. By dividing the initial ETF by the monthly reduction of $10.00, the total life of the ETF is 32.5 months for AT&T and 35 months for VzW. These implied ETF lives are at odds with the fact that the term of the typical subscriber contract is 24 months.

Recalculating the monthly ETF amortization based on a life of 24 months yields amortization rates of $13.54 for AT&T and $14.58 for VzW. In my view, the differences between the recalculated ETF amortization rate and the actual amortization rate, which are $3.54 ($13.54 less $10.00) and $4.58 ($14.58 less $10.00), constitute an interest payment. Furthermore, I see the device subsidy as nothing more than a loan made by the carrier to the consumer for the purchase of the wireless device. The handset subsidy is a loan that is repaid over the life of the subscriber contract. If the contract isn’t terminated, then intuition would tell us that the implied annual interest rate on the loan should be zero percent.

Shown in Table 4 is the financial impact and implied annual rate of interest that is experienced by an AT&T subscriber choosing to terminate service early, under the terms and conditions described in the subscriber contract currently used by AT&T today (For the purpose of establishing a reference point for comparison, I also provide the calculation showing the financial impact if the subscriber contract is not terminated early.)

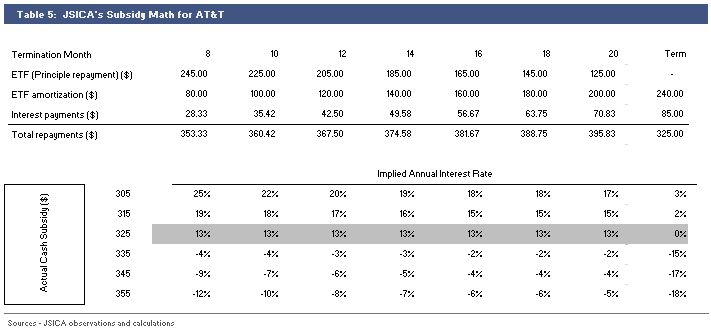

Table 5 presents the same calculation, which I call the JSICA Calculation, assuming that the subsidy is actually a loan. Under this scenario I add the amount of the difference between the recalculated amortization rate and the actual amortization rate in the form of interest payments.

Looking back at the implied subsidies I calculated in Part 2 of this series, AT&T and VzW would like consumers to think that the subsidies are generous and in many cases exceed the amount of the ETF. While subsidies are large, it is unlikely that on average, actual cash subsidies exceed the ETF for either company. Because of this, I calculate the implied interest rates assuming actual cash subsidies that revolve closely around the AT&T and VzW initial ETF amounts, rather than using the implied subsidy numbers found in Table 1 of Part 2 in this series.

Tables 6 and 7 show the same set of calculations as in Tables 4 and 5 but using the terms and conditions found in the VzW subscriber contract.

AT&T and VzW would probably disagree strongly with the analysis but I think this methodology is sound. The reason for this belief is that the JSI calculations pass the “aw, shucks” test. The results of the AT&T and VzW math produce nonsensical answers, whereas the JSICA calculations produce results that are predictable and just seem to make common sense. The best example of the difference between the two sets of calculations is the scenario where the actual cash subsidy matches the ETF. If the contract runs to term intuition tells us that the implied annual interest should be zero percent; this is exactly the result found in both sets of JSICA calculations. On the other hand, the AT&T and VzW calculations produce annual interest rates of negative 14 and negative 17 percent. Unless you believe in the tooth fairy, Santa Claus and that there really is such a thing as a free lunch, these results simply don’t hold water. In Part 4 of this series on Handset Subsidies and the Consumer Conundrum, I’ll explain why.

Dave Selzer

Dave Selzer