4G Offerings Will Further Dampen Wired Broadband Growth

Time was the term “cord-cutter” referred to the nearly 30% of Americans who have cancelled their landline voice service, relying solely on their wireless phone for voice communication. In response to this trend, for a decade or more, ILECs and RLECs nationwide have invested in broadband and video technology, looking to build communications bundles that will create “stickier” customers and generate incremental revenue as an offset to the decline in landline voice accounts.

More recently, we hear “cord-cutting” associated with those consumers who are cancelling their subscription video services, opting instead to rely on “over-the-top” (OTT) video solutions like those offered by Hulu and Netflix. Admittedly, most of the research indicates that the actual number of video cord-cutters remains low, but the trend has both the cable and ILEC industries worried—and, we think, for good reason. Generational differences in the habits of younger consumers are sure to perpetuate video cord-cutting, and the Great Recession may have accelerated the shift. (For more on generational segmentation, refer to our Mindshare article in the September, 2010 issue of The ILEC Advisor). But with 4G wireless service now a reality in dozens of cities nationwide, and based on the data we’ve collected regarding price and speeds, we’re now concerned that broadband access will be the next communications industry segment to be associated with the dreaded “cord-cutter” label.

Granted it’s the early days for the latest generation of mobile wireless services, but following an exhaustive survey of major 4G services now available and a comparison of prices and data speeds with wired broadband solutions, we’ve come to the sad conclusion that, while wireless can never (never say never?) be a complete Internet access substitute (due, for now, to spectrum constraints), broadband cord-cutting is likely to become an increasing reality. It will begin to happen over the next couple of years in major markets where Sprint/Clearwire, Verizon, MetroPCS and others have already launched 4G, and, over time, it could happen in all but the most rural markets nationwide. AT&T, which hasn’t even launched a 4G offering yet, reported more than 7.8m ‘connected device’ subscribers at the end of the third quarter, and Clearwire had 2.8m at that time and projects 4m subscribers by year-end—up from initial 2010 guidance of just 2m.

We’re not suggesting that a majority of broadband Internet subscribers will cut the cord tomorrow and opt for a 4G solution instead, but considering that wired broadband penetration gains have not accelerated for two years now, we think the advent of 4G wireless options will simply further retard growth. That combined with the Net Neutrality rules the FCC is voting on today (12/21), which have more relaxed regulations for wireless providers (this is why Verizon’s lawyers and lobbyists make the big bucks!), will make wireless broadband a force to be contended with in coming years.

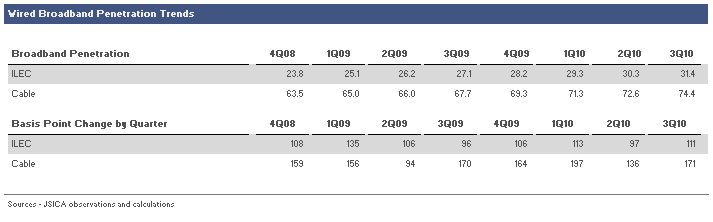

Wired broadband penetration has been creeping higher quarter by quarter, but for the public ILECs that we track, the growth has been modest. In 3Q10, broadband penetration of ILEC access lines rose 111 basis points, to 31.4%. But if you consider that the number of voice lines has been falling each quarter, the “growth” is really minimal. Cable broadband penetration (calculated as broadband connections/ basic cable subscribers) rose 171 basis points, to 74.4% over the same period. Here too, the denominator is shrinking, overstating somewhat the increase in overall broadband customers. The public cable companies have lost more than half a million subscribers in each of the past two quarters.

At the end of the day, consumers will evaluate the value proposition offered by wireless broadband providers, and go where they get the most bang for their buck. Data speeds matter, but the new wireless offerings appear to stack up reasonably well with all but the fiber-based offerings like FiOS—and we believe there may already be more homes passed nationwide by 4G offerings than by fiber-to-the-home services.

At the end of the day, consumers will evaluate the value proposition offered by wireless broadband providers, and go where they get the most bang for their buck. Data speeds matter, but the new wireless offerings appear to stack up reasonably well with all but the fiber-based offerings like FiOS—and we believe there may already be more homes passed nationwide by 4G offerings than by fiber-to-the-home services.

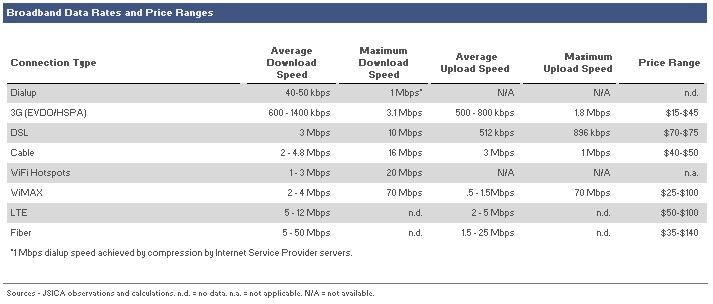

Furthermore, the price/ value propositions are compelling. At the low end, a Clearwire Base Home service can be had for $35/ month and the average WiMax speeds are competitive with DSL—for which the average ILEC was generating $70 or more per broadband sub per month based on a study of monthly ARPU we conducted last spring.

Broadband cable revenue is generally lower per user—in the $40-$50 range—and the speeds are competitive with WiMax. Simple lethargy and attachment to those subscription video services will prevent those customers from changing provider rapidly, but in the long run those seeking to replace their $80/ month video package with Netflix’ $9/ month streaming option may opt to end the relationship with their cable provider. We don’t believe this happens quickly, but Clearwire’s rapid subscriber growth demonstrates a certain amount of pent-up demand. Ironically, cable providers Time Warner and Comcast are partners in Clearwire and are bringing some of that wireless broadband subscriber growth to the company.

LTE speeds are even stronger than DSL or cable, but the price points are generally higher and metered pricing is likely to become a bigger factor as these new networks are loaded up. Will the consumers place a premium on mobility? Some will; early adopters and road warriors with their tablet devices will be the first to try the new services; over time those of us who’ve gotten used to tapping 3G networks via our smartphones will decide it’s time for a faster connection.

The device selection for LTE networks remains limited, and somewhat expensive, but as with everything, those prices will fall. Verizon, which launched its LTE network on December 5, 2010 with just two USB modem options, will have LTE handsets in volume by the middle of next year.

And let’s not forget about “Apps.” The major wireless carriers are taking a proactive interest in attracting developers to create the type of applications that have fueled the iPhone’s popularity. With data speeds averaging between 5 Mbps and 12 Mbps, some pretty cool apps are possible over the LTE network. (I tested my data speeds online while writing this article and found that I’m working with a dismal 1 Mbps download speed and 250 kbps upload speed—and I still manage to view the Youtube videos my mother emails regularly!)

As mentioned above, spectrum issues are the most obvious constraint to wireless carriers as their 4G networks load up, but we don’t underestimate the ability of the industry’s suppliers to engineer more and more capacity out of limited airwaves. At the same time, the FCC is planning to auction more spectrum and some carriers—Clearwire most notably—have excess capacity and are looking to sell off some chunks in order to raise cash.

The bottom line? We think it’s still a long time coming—especially in rural markets—but we think the ILEC industry would be ill-advised to discount the long-term ability of next-generation wireless broadband offerings to cut into its revenue growth. Those investing in fiber networks will benefit from the explosion in backhaul needs, but DSL growth potential is unquestionably limited if you look out beyond the next decade. And while fiber-based services will compete favorably with wireless broadband, particularly in the enterprise market, not all markets will provide a satisfactory ROI on fiber deployments.

Richelle Elberg

Richelle Elberg