Consolidated/Enventis Merger a Strategic Fit

The Deal

On June 30, 2014, Mattoon, IL-based Consolidated Communications announced it would merge with fellow publicly-traded ILEC, Minnesota-based Enventis (formerly HickoryTech) in an all-stock transaction valued at $350 million. At the deal’s targeted close in 4Q14, Enventis shareholders will receive 0.7402 shares of Consolidated stock for each Enventis share—an implied value of $16.50 on announce date.

During the past year, Consolidated CEO Bob Currey had indicated on earnings calls that CNSL would be open to deals if a property with right mix of assets hit the market. Behind the scenes, Consolidated already had its sights set on Enventis.

According to the proxy statement filed with the SEC, Currey and Enventis CEO, John Finke began discussing a possible transaction in June 2013, a year before the merger’s eventual announcement. Consolidated’s initial merger proposal--offered on June 29, 2013--valued Enventis shares at $12.50, approximately 25 percent below the announced deal price. The parties engaged in talks on-and-off over the next year negotiating terms—fixed vs. floating share exchange rates, number of board seats (Enventis wanted 2, got 1), and termination fees ($8.5m) among others.

Strategic Considerations

Strategically, the merger makes sense as both companies have employed similar growth strategies over the last several years, focusing on enterprise-centric, broadband services. Consolidated acquired SureWest in 2012, picking up FTTH-based networks in Kansas City and California. HickoryTech, which officially changed its name to Enventis in April, acquired network provider Enventis Telecom in 2005 and added Fargo, ND-based IdeaOne in 2012 further expanding its fiber network. Although the companies do not have contiguous footprints, their operations are both largely centered in the Midwest.

The proxy statement indicates that Enventis’s management and board considered other strategic alternatives, but determined a merger with Consolidated was in the best interest of its shareholders. In the board’s estimation, Consolidated was the most strategic acquirer and that Enventis was unlikely to fetch a higher price through an auction due to the limited number of strategic buyers and the lack of synergies present for financial buyers.

Financial Highlights

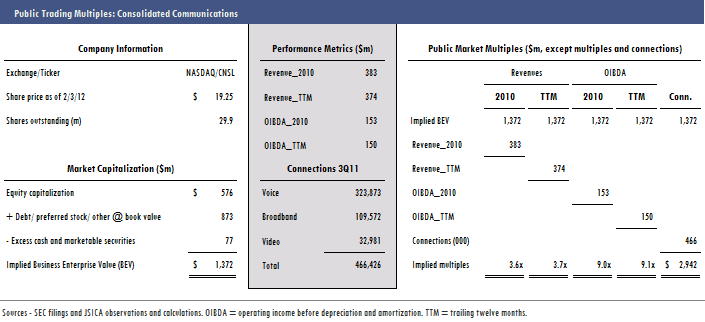

The deal values Enventis at implied multiples of 1.9x trailing revenue, 7.3x trailing OIBDA and 5.6x pro forma OIBDA factoring in $14m in annual operating synergies. By comparison, Consolidated paid just 6.3x trailing and 4.8x pro forma cash flow for Surewest, indicating that the market for wireline telecom has stabilized during the past few years.

Structuring the deal as an all-stock merger allows Consolidated to delever its balance sheet. Factoring in synergies, Consolidated’s debt to OIBDA ratio will decline from 4.3x to 3.9x. Additionally, the all-stock transaction frees up cash to invest in success-based capital projects including near-net opportunities on Enventis’s 4,200 mile fiber network.

Closing Thoughts

While Consolidated touts the organic growth opportunities granted by the merger, the truth is that delivering meaningful organic growth is difficult, and M&A remains the primary driver of growth for wireline telecom providers. Consolidated has grown revenue from $349m in 2011 to $601m in 2013, but pro forma the SureWest acquisition, its revenue has actually declined year over year since 2011. With shareholder pressure to maintain dividends and to keep stock prices elevated, another year of limited top-line growth is a difficult narrative to sell—M&A tends to offer a more compelling story. Now the ball is in Consolidated’s court to translate the Enventis merger into value for its shareholders.

Adam Brissette

Adam Brissette