Altice Pays $17.7b for Cablevision, Doubles Down on U.S. Cable

French telecom firm Altice announced on Thursday, September 17th that it had agreed to acquire Cablevision Systems Corporation (NYSE:CVC) at a headline price of $17.7b, or $34.90 per share. The deal comes on the heels of Altice’s May purchase of Suddenlink for $9.1b, which marked its entrance into the U.S. cable market. The combination of Suddenlink and Cablevision represents the 4th largest cable operator in the U.S. and continues the trend of large-scale M&A amongst U.S. cable operators.

Valuation Analysis and Deal Metrics

Transaction Facts

- BC Partners and CPP Investment Board, from which Altice acquired its 70 percent stake in Suddenlink, have an option to participate for up to 30 percent of the equity of Cablevision

- $900m in annual synergies anticipated

- Expected close 3Q16-4Q16

Strategic Considerations

- Provides greater scale to realize cost synergies across Suddenlink and Cablevision

- 65 percent take rate of triple play services drives industry-leading ARPU of $155

- Highly competitive network that is 100 percent digital, offering triple play--video, broadband and VoIP—throughout service area

JSICA’s Take

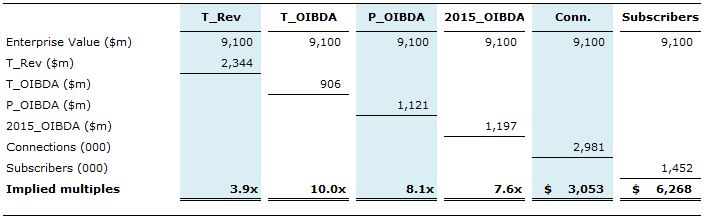

After Altice scooped up Suddenlink in May, we indicated that more U.S. cable deals were on the horizon for the acquisitive French telecom giant. Cablevision, an oft-rumored takeover target in recent years, was a logical target. At multiples of 2.8x trailing revenue and 6.9x pro forma EBITDA, Cablevision was less expensive than Suddenlink (3.9x revenue/8.1 pro forma EBITDA)—the discount largely attributable to Cablevision’s inability to deliver meaningful revenue and EBITDA growth over the past five years.

Existing high penetration rates and strong in footprint competition from Verizon will make it challenging for Altice to accelerate Cablevision’s top line growth, but founder Patrick Drahi is confident that between network modernization, the streamlining of operations and consolidation of management, there is ample room for cost savings--$900m worth to be exact.

The deal marks continued consolidation of U.S. cable/broadband providers in 2015, particularly amongst mid-sized operators. Deal multiples averaging a lofty 3.6x revenue and 8.0x pro forma cash flow could entice the remaining regional/mid=sized cablecos to sell. And with Altice looking to increase its overall revenue mix to 50 percent from its U.S. operations, there is at least one motivated buyer in the market.

Deal Advisor, Deals: CATV

Deal Advisor, Deals: CATV