zColo Pays $15.9m for Las Vegas Data Center

Zayo Group Expands West Coast Presence

zColo, a Zayo Group Company, announced on January 3rd that is has acquired all of the net assets of MarquisNet, a Las Vegas-based co-location provider. According to documents filed with the SEC, zColo will pay approximately $15.9m in the deal, subject to post-closing adjustments. The purchase was funded through Zayo’s revolving line of credit, which prior to the deal was $63.3m. MarquisNet represents Zayo’s 18th acquisition since its inception in 2006.

The primary asset in zColo’s purchase is MarquisNet’s data center, located at 7185 Pollock Drive in Las Vegas. The facility features 28k square feet of co-location space, Tier 1 Internet access, N+1 routing equipment and HVAC redundant design. Including this newly acquired facility, zColo owns and operates 12 data centers in 11 markets including Los Angeles, New York and New Jersey. Zayo Group, zColo’s parent company, has indicated that it will extend its fiber network to 7185 Pollock Drive, joining AT&T, XO, Cox Communications and Sprint among the nine carriers that have a fiber connection to the facility.

The acquisition of MarquisNet and the forthcoming fiber build into the Las Vegas facility furthers Zayo’s efforts to expand its presence out West. In December, Zayo closed on its $393m purchase of 360networks, which provided it with access to a number of new markets on the West Coast including Albuquerque, San Francisco and Tucson. It also recently completed a fiber build into the Green House Data Center in Wyoming, providing the facility with metro and long haul connectivity, and it is in the middle of a fiber network build in San Diego.

zColo commented in its press release announcing the MarquisNet purchase that among its enterprise clients there has been a surge in demand for data centers as a location for disaster recovery on the West Coast. Las Vegas in particular is a popular destination for data center owners to build and operate thanks to its cheap land, and relative lack of natural disasters. Data center specialist Switch operates multiple properties in Las Vegas including its flagship 400k square foot SuperNap facility and it will soon break ground on a $400m project to add 600k square feet of data center space in Las Vegas. Both Zayo and Switch attribute the increase in data center demand at least in part to the increase in cloud computing.

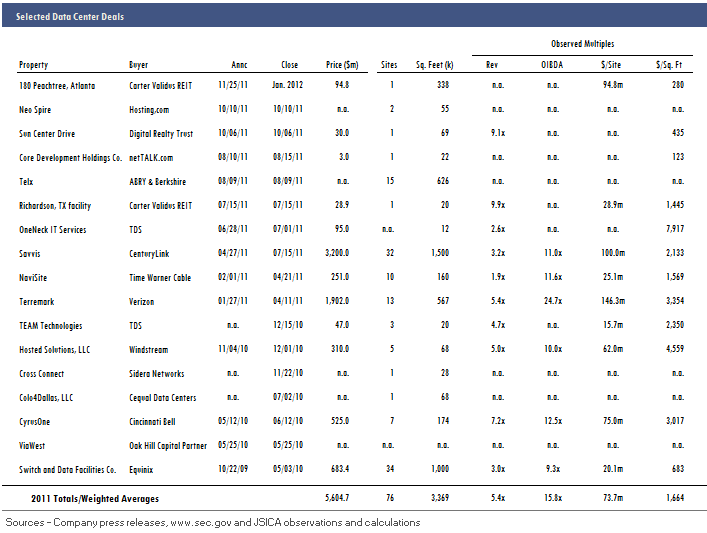

At a price of $15.9m, zColo paid approximately $568 per operating square foot for MarquisNet, a multiple below the average price of $751 per square foot observed in recent transactions. We have no past financial information on MarquisNet, however recent data center deals have been struck at an average of 5.7x revenue which would indicate the facility could add around $2m-$3m to zColo’s top line. Based on its 3Q11 financials annualized, zColo currently generates approximately $39m in revenue annually.

Deals: Data Centers

Deals: Data Centers