Refaire Le Monde: Sprint + CenturyLink = Giant Slayer?

If AT&T/ T-Mobile Goes Through (Even If It Doesn’t), This Deal Makes Sense

Should CenturyLink (NYSE:CTL) acquire Sprint (NYSE:S)? There’s been a good deal of speculation in recent weeks that Sprint may need to sell in order to stay competitive should the proposed AT&T (NYSE:T)/ T-Mobile deal go through, speculation that was confirmed by ceo Dan Hesse’s own testimony before Congress earlier this month. Numerous analysts have suggested that the most logical buyer of Sprint would be CenturyLink, which is now the #3 wireline company nationwide, following its buy of Qwest (that deal closed April 1). CenturyLink (then CenturyTel) exited the wireless business back in 2002 when it sold its wireless operations to Alltel (now part of Verizon, NYSE:VZ).

In this installment of Refaire Le Monde (literally, to “remake the world”), I’ve done an in-depth analysis of where CenturyLink stands today, pro forma its recent Qwest buy as well as the pending Savvis (Nasdaq:SVVS) data center buy, and what the company might look like if it swallowed Sprint. While CenturyLink ceo Glen Post did note in the company’s recent quarterly earnings call that the company is focused on integrating what it’s got for now, I don’t think for a moment that Mr. Post, who has proven himself VERY adept at making large acquisitions and creating shareholder value, isn’t looking out to 2012 and beyond, and seeking a way to bring a wireless play back into the fold.

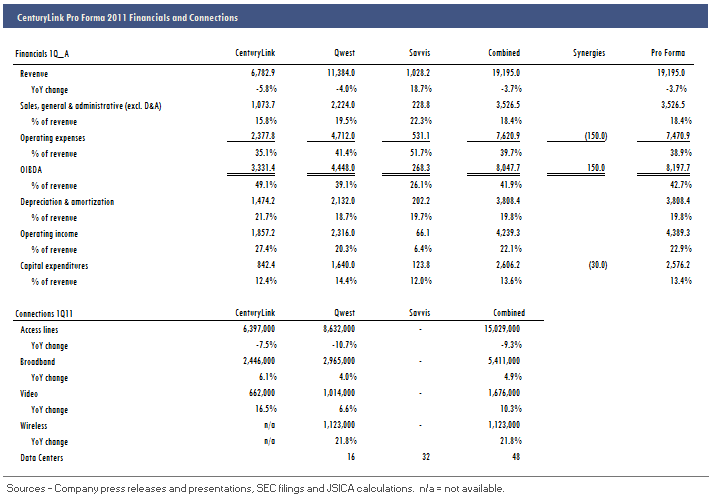

First, let’s see where CenturyLink will be pro forma its recently completed/announced buys. Using annualized first quarter 2011 results I’ve come up with a pro forma 2011 P&L. Because Qwest didn’t close until April 1, and Savvis won’t close until later in the year, CenturyLink’s actual guidance for 2011 calls for about $15b in revenue—but Wall Street is always looking ahead and discounting anticipated results.

What Wall Street sees when it looks at CenturyLink today is a company that will have more than $19b in revenue going forward, up from actual 2010 results of about $7b. OIBDA on a combined basis, before any synergies, would be about $8b, for a 42% margin. The company will have more than 23m connections, including about 1.1m wireless connections it picked up from Qwest, and 48 data centers in the U.S. and abroad. Longer-term, the synergies expected from integration of Qwest are much higher, but for year one we’ve assumed $80m from Qwest and also factored in the $70m in anticipated Savvis synergies. That bumps up run-rate OIBDA to about $8.2b, and another $30m in capex savings from the Qwest deal are expected this year.

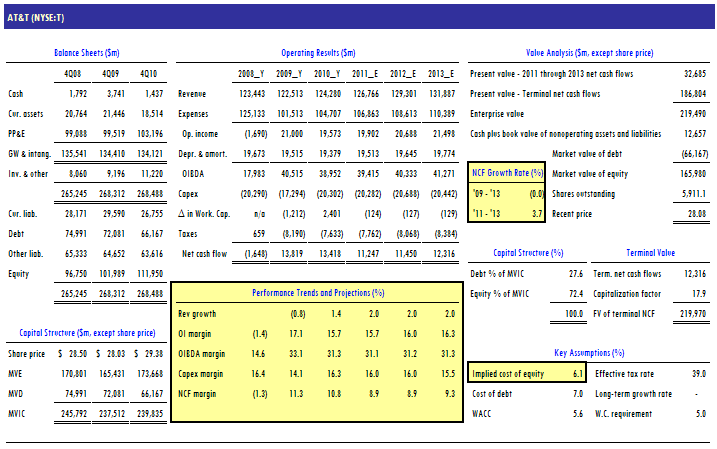

So how does it compare with AT&T and Verizon at that point? Still pretty small potatoes. Based on annualized first quarter results, AT&T’s top line is running at about $125b (6.5x my pro forma estimate for CenturyLink) and Verizon was at $108b (5.6x CenturyLink). And where CenturyLink had more than 23m connections including Qwest, AT&T had more than 161m and Verizon had nearly 142m. Should AT&T be allowed to acquire T-Mobile, its total connections as of 1Q11 would have been more than 195m!

Now, let’s see what CenturyLink would look like if combined with Sprint too. Total connections would exceed 75m—that includes 51m wireless subscribers as well as 8m local lines that Sprint’s wireline division serves (more on that in a moment). Pro forma annualized first quarter results would have been about $52.5b in revenue—still less than half of either AT&T or Verizon.

Needless to say, I don’t see how regulators could deny the combination—even if they do ultimately axe the T-Mobile deal (which still seems unlikely, but I have to admit that the groundswell against the deal is gaining momentum and could in fact have an impact in the end…but I digress).

Clearly the biggest benefit to a Sprint buy is its more than 50m wireless subscriber base and spectrum holdings. The company is presently undertaking a major network overhaul that will eliminate the Nextel iDEN system over the next several years. It will cost upwards of $5b but the company believes that major cost savings will result, not to mention it will free up 800 MHz spectrum for new technology deployment, like LTE. Since he took the helm in early 2008, Dan Hesse has accomplished an impressive turnaround, and while the company isn’t out of the woods yet, it did manage to grow its subscriber base by 1.1m in the first quarter--its best growth in five years--even in the face of the Verizon iPhone. Both churn and ARPU have been improving, which raises the quality of the subscriber base, and Sprint has several B2B and M2M initiatives underway.

One thing not often mentioned in any discussion of Sprint, however, is its relatively large wireline operation. The company does about $1.2b per quarter in wireline revenue and wireline OIBDA in 2010 was nearly $1.1b. Sprint markets local voice, data and Internet service primarily to business customers, and the company’s web site says, “Currently, Sprint manages more than 8 million local phone lines—a number that grows every year as our local phone service footprint expands.”

“Sprint provides a comprehensive menu of local business communications packages for customers in our local service areas that includes calling features, domestic long distance, and Internet services. In addition to these local services, Sprint also offers integrated wireless and data services. Many of the most popular services and features are available in packages at discounted rates or can be purchased individually.” The company’s 10-K describes the network as “an all-digital global long distance network and a Tier 1 Internet backbone.” Based on the 8m line figure and trailing revenue, Sprint generates about $52/line/month in its wireline division.

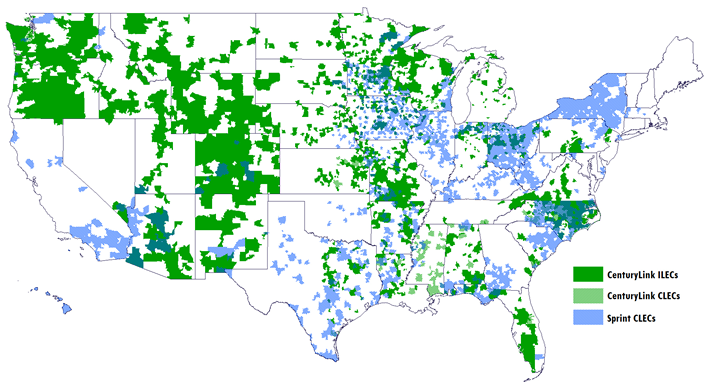

A map of Sprint’s CLEC markets shows the extensive coverage as well as a minimum of overlap with CenturyLink’s ILEC and CLEC markets. CenturyLink’s goal of becoming less dependent upon consumers also fits well with Sprint’s existing focus on business markets—also an area the company has recently refocused on with its wireless offerings.

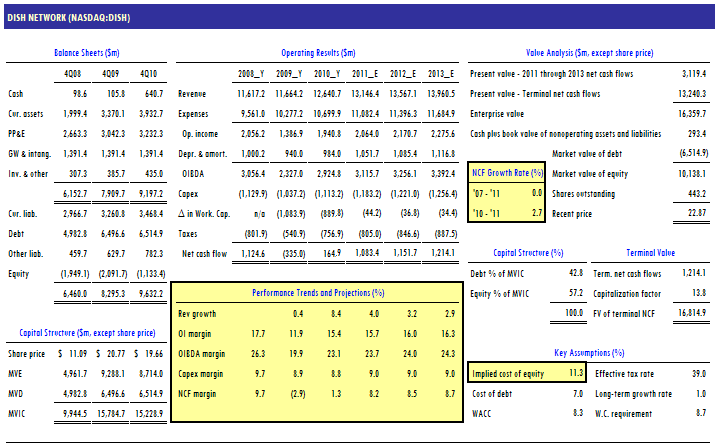

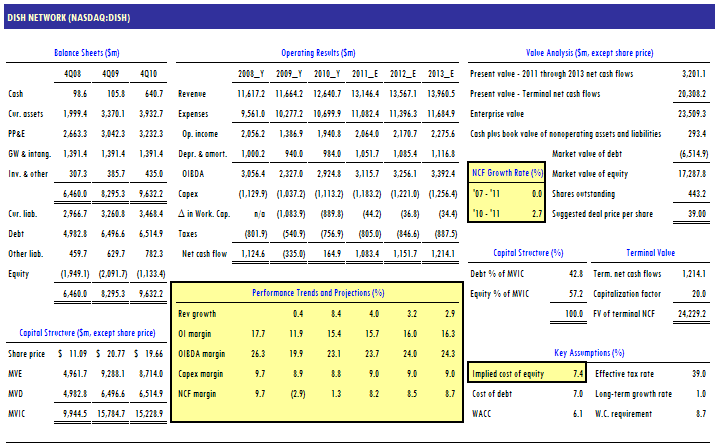

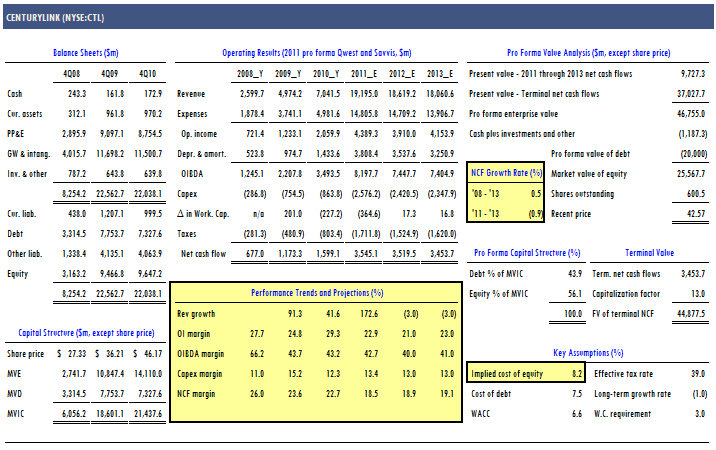

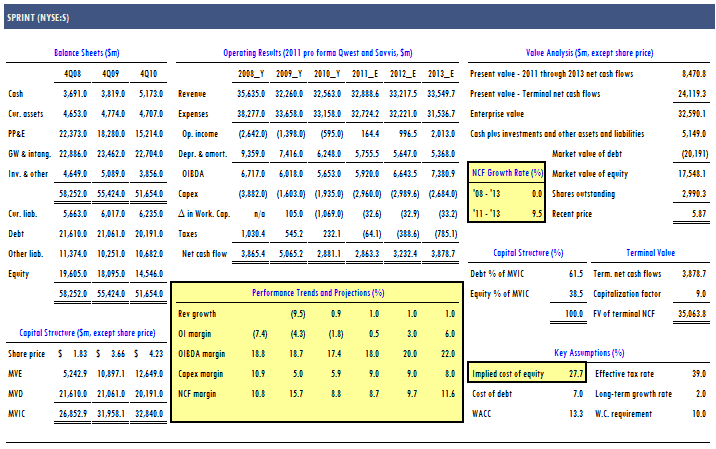

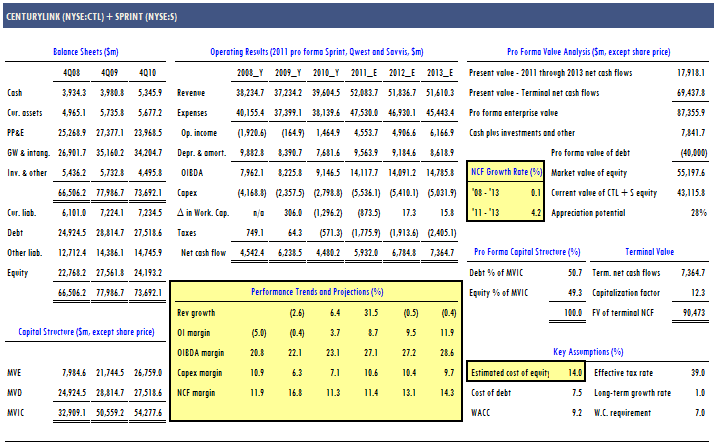

So what about capitalization and valuation? First I ran separate Discounted Future Income (DFI) analyses on both CenturyLink and Sprint to see what the market is requiring today in terms of equity returns and what the public valuations imply. For CenturyLink I used my pro forma 2011 revenue and expense figures, although admittedly, the company won’t actually generate $19b this year. I then projected 2012 and 2013 results for CenturyLink in its current configuration (including Savvis). Due to continued access line losses, the top line could fall to just $18b by 2013, despite growth in the to-be-acquired data business. Net cash flow is also projected to fall, albeit slowly. Based on my expectations for capitalization and using a 7.5% cost of debt, CenturyLink’s current trading price indicates that Wall Street requires a relatively modest 8.2% rate of return on equity. The implied enterprise value is $46.8b, or 2.4x pro forma revenue and 5.7x pro forma OIBDA.

Next I ran a similar analysis on Sprint. Shares in Sprint have risen impressively in recent months—some of that may be related to deal speculation, but there’s no doubt that the company’s turnaround (Clearwire woes notwithstanding) is also having an effect. Despite plans for higher capital investment over the next few years, Sprint’s free cash flow should grow fairly rapidly, especially once the benefits of the Network Vision overhaul kick in. That assumes, of course, that Sprint can continue to grow its subscriber base. It looks to me like the market is valuing Sprint at about $32.6b these days—less than 1x revenue—and demanding an equity rate of return of nearly 28%. That’s an improvement over last year, however, when a similar analysis showed that the market needed more than 31% to invest in Sprint shares.

So, what happens when you combine the companies? Several things of significance, even before cost synergies can be factored in. The debt/ cash flow ratio for Sprint falls—it’s at about 3.4x now. I figure a combined Sprint/CenturyLink would have a debt/ cash flow ratio around 2.8x. The growth profile of the combined companies also improves dramatically. In my mind, this translates to a much less aggressive required rate of return on equity. Using 14%, and with no synergies yet built into the model, my DFI analysis indicates that CenturyLink-Sprint would be worth more than $87b and have an equity value of more than $55b. In comparison, the current combined public equity value of the two companies is about $43.1b—indicating the potential for a 28% gain. Synergies could make that even higher, although the 1% perpetuity growth rate I’ve estimated is highly dependent upon Sprint’s continued success in growing its subscriber base—something the company says would be threatened by an AT&T acquisition of T-Mobile. Despite Dan Hesse’s very public outcry, however, I tend to think that Sprint would have a good opportunity to steal a lot of T-Mobile’s existing subscriber base as they are forced onto higher-priced AT&T price plans.

At the end of the day, Glen Post will likely stick to his knitting for the immediate future, and observe with interest as the AT&T/ T-Mobile discussion takes place in Washington. But regardless, a telecom company today needs a wireless play (said the 20-year wireless industry analyst) if they intend to keep growing. Sure, there are other opportunities that beckon a wireline company, but let’s face it, wireless is where the greatest upside remains, and Post has a solid history of buying for growth (except maybe that wireless division sale back in ’02). I think the combination makes sense and I don’t see how Washington could deny it given the size of the two largest competitors. The biggest question now isn’t really IF but WHEN.

Richelle Elberg

Richelle Elberg