Towerstream Makes Largest Buy to Date

Fixed Wireless Provider Expands in Los Angeles

Middletown, R.I.-based wireless broadband provider Towerstream Corp. (Nasdaq:TWER) announced October 31, 2011 that it has entered into a definitive agreement to acquire certain business assets from Los Angeles-based Color Broadband, in a transaction comprised of cash, common stock and assumed debt. Towerstream will acquire all customer contracts, network infrastructure and related assets of the fixed wireless service provider, and is expected to close the deal by the end of the year.

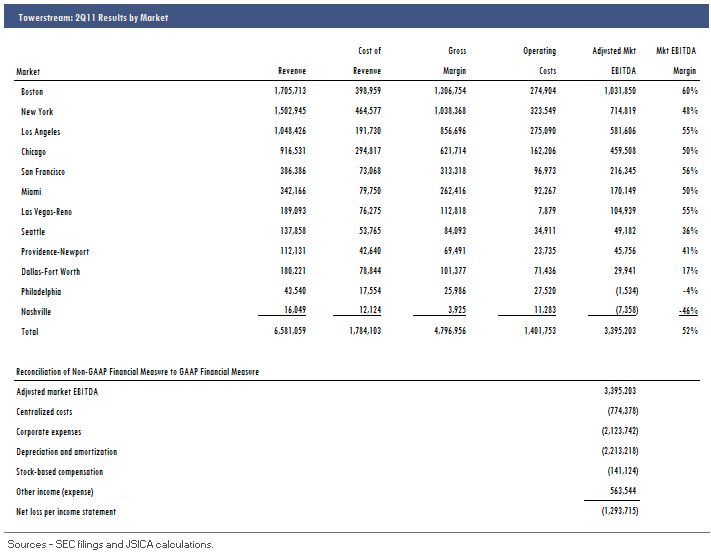

It’s Towerstream’s fourth buy over the past two years, and also the largest to date. The value of the deal was not disclosed, but the biggest deal prior to this announcement was for nearly $3.5m. Towerstream said that the Color Broadband business will increase its L.A. market revenue by 70%, implying annual revenue for the target of around $2.8m. That's based on the $1m Towerstream did in L.A. in 2Q11, as reported in the company's 10-Q. It’s still tough to guesstimate the deal value, however. While Towerstream trades for more than 5x revenue presently (see below), it paid just 1.2x revenue when it acquired the fixed wireless operations of Chicago-based Sparkplug in April of 2010.

Arguably, Towerstream is still in ramp-up mode, which justifies the relatively high trading multiple. The company has posted little in the way of positive cash flow over the past year, but is still actively seeking and building acquisition markets. At the end of 2Q11, Towerstream was serving an estimated 3,200 business customers with its fixed wireless solution, in a dozen markets.

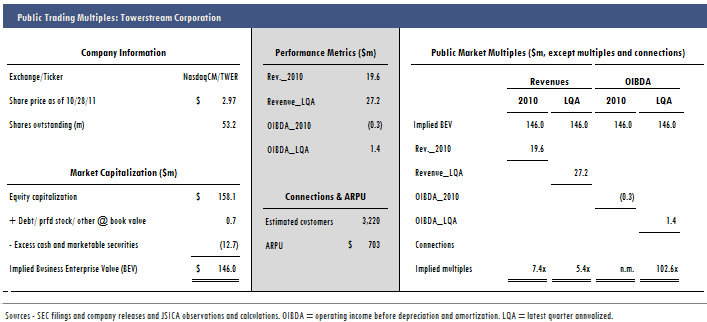

Based on Towerstream's closing price on October 28, 2011, and backing out the company's substantial working capital surplus (some of which may now be committed to the Color Broadband deal), the market is valuing the company at about $146m, or 5.4x run-rate revenue. Based on the healthy margins reported in its more mature markets there may be a good deal of upside to the company's cash flow--IF it can maintain market share.

But it seems that everyone and his brother is going after the broadband and business markets these days; in order to hit those promising cash flow targets, Towerstream's wireless solution (which relies on both licensed and unlicensed spectrum as well as WiFi) will have to increasingly compete with fiber-based competitors. My guess is that the company is able to compete effectively on price--a wireless solution is generally cheaper than fiber--but the question will become one of capacity and speeds over the longer term.

Richelle Elberg

Richelle Elberg