Leap Wireless and Verizon Wireless Announce Spectrum Deals

Is a Spectrum License Land Grab in the Offing?

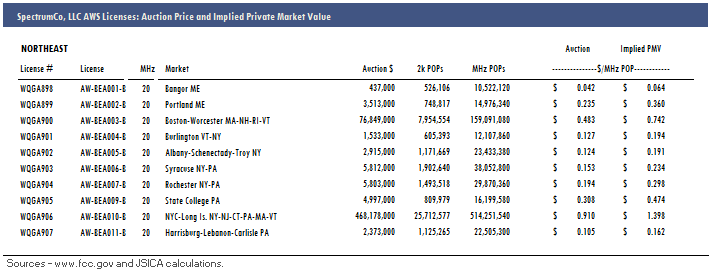

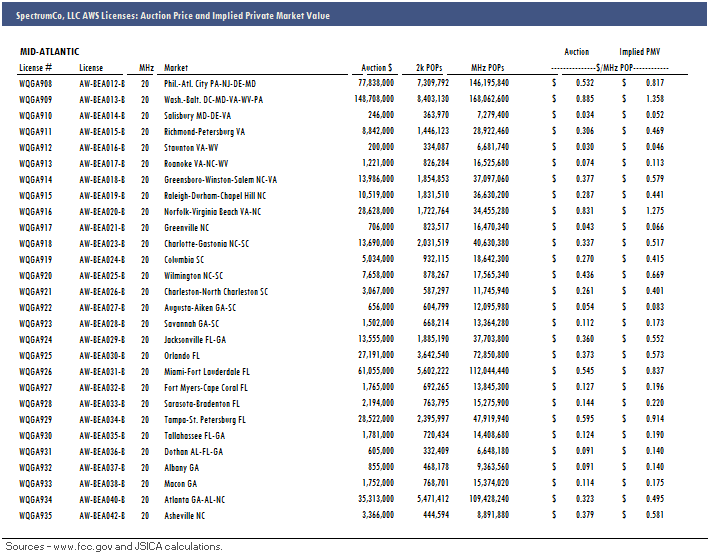

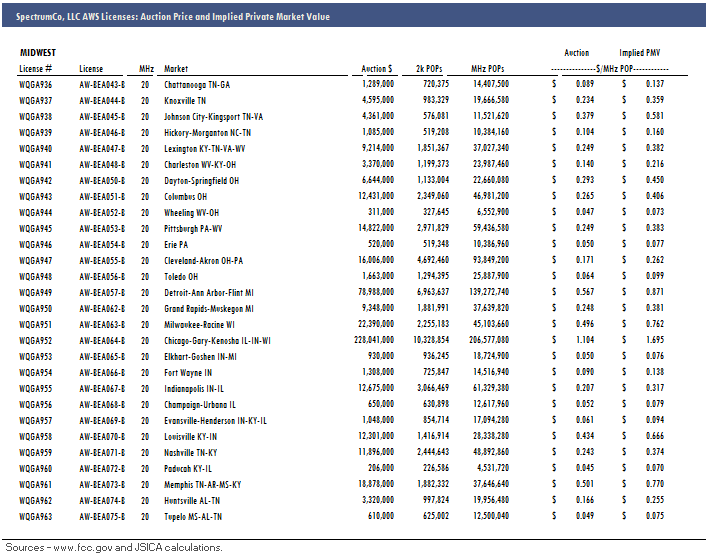

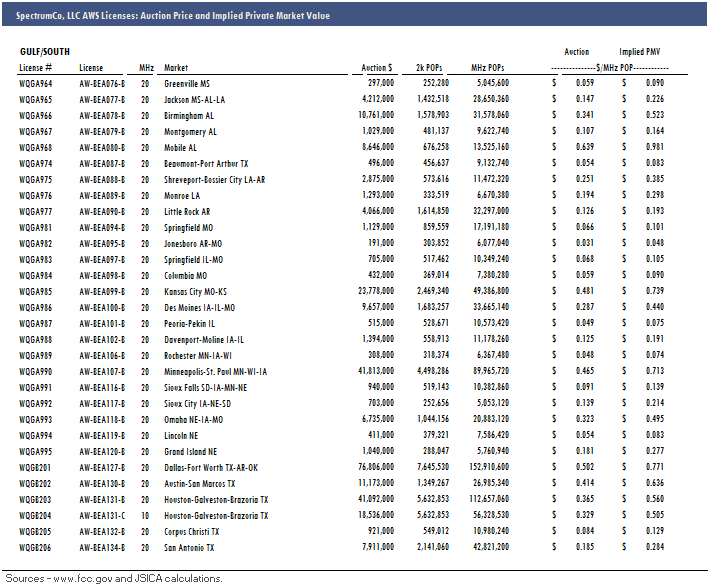

Last week Verizon Wireless and the cable consortium known as SpectrumCo announced a $3.6b deal for AWS licenses covering 259m POPs; that deal implied a more than 50% increase in the value of the subject licenses since the 2006 FCC auction. This week, Verizon is back at the table, acquiring $360m worth of PCS and AWS licenses from Leap Wireless and Leap affiliate Savary Island. In exchange, Verizon is selling 12 MHz of 700 MHz spectrum covering nearly 11m POPs in Chicago to Leap, for $204m.

Both deals indicate a healthy increase in spectrum values—which doesn’t come as a surprise given the growing popularity of mobile broadband services and the carriers’ race to deploy 4G LTE service. I also see AT&T’s March announcement that it would (attempt to) acquire T-Mobile as well as AT&T’s December 2010 deal for $1.2b in Qualcomm spectrum as catalysts that prompted Verizon to start shopping more seriously.

It’s potentially the beginning of a real land grab for spectrum licenses; those who 'have' will benefit from the major projected increase in mobile broadband use, and those who ‘have not’ could well be left behind. Those who 'have and sell' might earn a nice return today, but that leaves open the question of how to participate in the coming hockey stick growth pattern. The good news is that it seems much of the long dormant AWS spectrum is going to emerge from its cocoon, providing options for ILEC license holders.

In the $204m deal for Chicago, Leap is paying nearly 34% more than Verizon spent at auction in 2008, or $1.58/MHz POP. Verizon paid $152.5m for that license.

Leap said in its Public Interest Statement filed with the FCC that the additional 12 MHz “is needed to supplement the 10 MHz of spectrum on which Cricket currently operates in the Chicago area. The additional spectrum will enable Cricket to deploy LTE technology and thereby expand its service offerings, strengthen its presence, and improve the quality of services available to consumers in Chicago.” It continues, “With carriers worldwide upgrading to faster and more efficient LTE technology, Cricket’s deployment of this technology is critical to its ability to deliver competitive services to customers in the coming years. The associated sale of PCS and AWS spectrum to Verizon Wireless also enables Cricket to substantially finance the purchase of spectrum in Chicago. This transfer will thus enhance competition by enabling Cricket to provide more consumers with access to a wider array of high quality wireless communications services.”

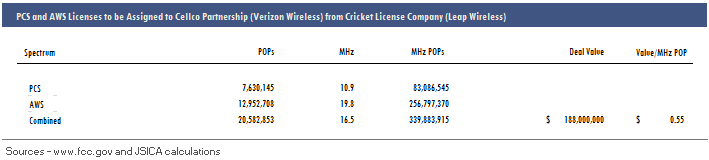

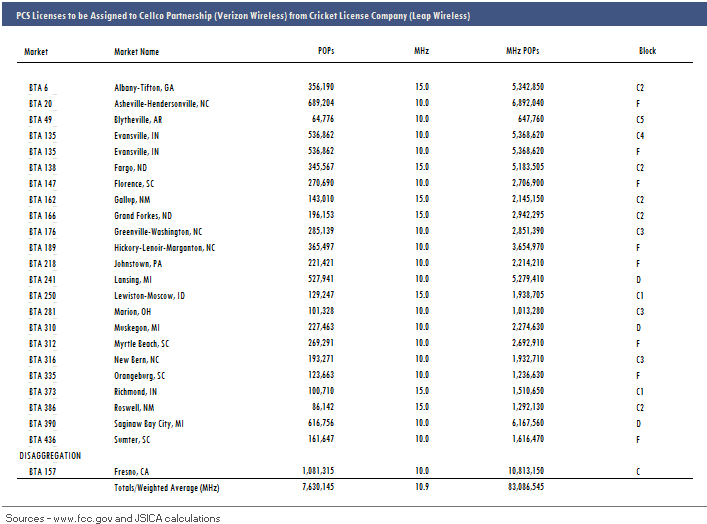

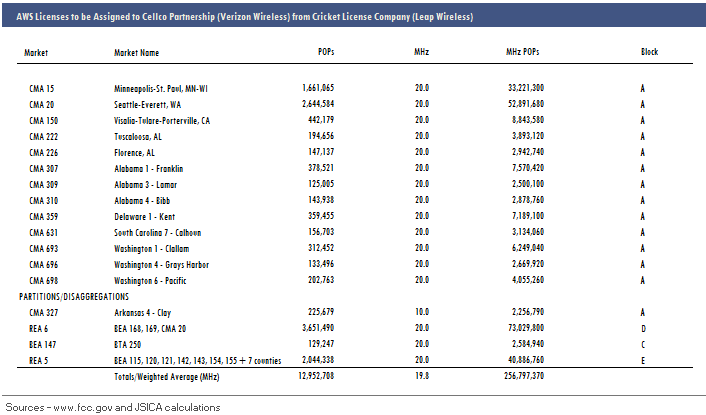

In the second transaction, Leap will sell nearly 340m MHz POPs comprised of both PCS and AWS spectrum licenses, for $188m, or $0.55/MHz POP, to Verizon. The licenses cover a total of 20.6m POPs and are scattered across the country.

Also in the Public Interest statement filed with the FCC, Verizon Wireless said that it “seeks to acquire spectrum to augment its existing capacity in order to respond to the projected increase in customers’ use of its network, particularly the rapidly growing customer demand for high speed wireless data services. Consumer demand for such services is exploding. Smartphone adoption continues to surge: 59 percent of mobile handsets sold in the United States in the third quarter of 2011 were smartphones, and currently 43 percent of all U.S. mobile phone subscribers own a smartphone. As consumers experience higher speeds through the use of smartphones, they tend to consume more data. Today, smartphones use 24 times more spectrum capacity than traditional phones. According to public estimates, the average smartphone will generate 1.3 GB of traffic per month in 2015 (a 16-fold increase over the 2010 average) and aggregate smartphone traffic in 2015 will be 47 times greater than it is today. Similarly, the rapid adoption of tablets places another substantial drain on spectrum. Tablets use approximately 120 times the capacity of traditional phones. In 2015, it is projected that mobile-connected tablets will generate as much traffic as the entire global mobile network in 2010."

Whoa Nellie! Smartphone traffic nearly 50x greater than it is today by 2015? And tablets will use as much traffic as the entire global network does today? Sounds to me like a serious demand for spectrum is brewing, which means values should continue to increase.

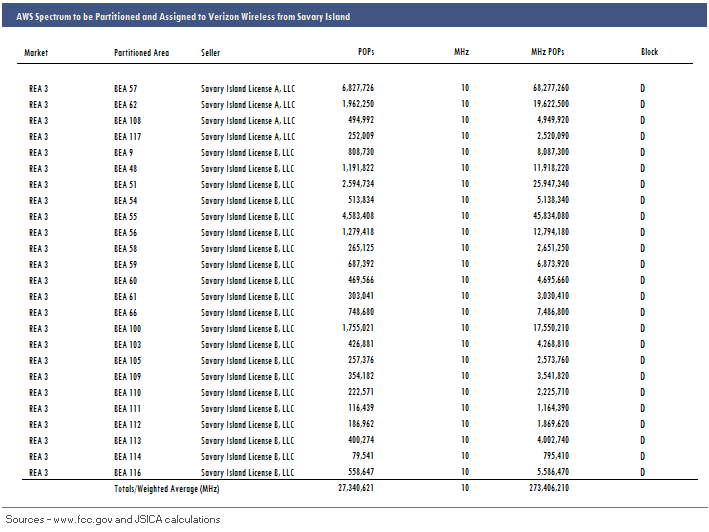

Finally, majority-owned (non-controlled) Leap Wireless affiliates Savary Island License A, LLC and Savary Island License B, LLC are selling an aggregate of 10 MHz of AWS spectrum covering 27.3m POPs to Verizon, for $172m or $0.63/MHz POP.

The receipts will be used to repay debt owed to Leap, which will in turn use the money to help pay for its Chicago 700 MHz buy and continue its LTE deployment.

The receipts will be used to repay debt owed to Leap, which will in turn use the money to help pay for its Chicago 700 MHz buy and continue its LTE deployment.

There's no doubt in my mind that we will continue to see the larger wireless carriers scoop up spectrum assets as the reality of the changing market sinks in. Verizon has been running its LTE network for a year now--clearly it's seeing a rapid increase in usage and as noted above, the tablet boom is only in its infancy. The question for you readers becomes how best to capitalize upon the opportunity.

There's no doubt in my mind that we will continue to see the larger wireless carriers scoop up spectrum assets as the reality of the changing market sinks in. Verizon has been running its LTE network for a year now--clearly it's seeing a rapid increase in usage and as noted above, the tablet boom is only in its infancy. The question for you readers becomes how best to capitalize upon the opportunity.

Richelle Elberg

Richelle Elberg