NetTALK Adds Revenue Streams with Data Center Purchase

VoIP Provider to Offer Cloud Hosting and Managed Services

NetTALK.com (OTCBB:NTLK.OB) is diversifying its services once again. A provider of VoIP services and products, netTALK.com has purchased a 22k square foot data center in Miami from Core Development Holdings Corporation for $2.7m. The Miami-based company’s acquisition is the most recent purchase in an extremely active data center market. Perhaps the most strategic asset included in the deal is a 150-foot, 4G enabled cell tower that will complement netTALK’s new business venture into wireless.

A registered CLEC in over thirty states, netTALK was founded in 2008 using a similar business model to the more publicized MagicJack. Its flagship device, the DUO, allows customers to connect their phones to the Internet from a computer, or directly through a router—a feature MagicJack lacks. NetTALK charges about $70 for the DUO and $30 per year for service—which includes unlimited voice minutes. While its annual revenues will likely surpass $2m in 2011, up sharply from just under $600k in 2010, the company continues to operate at a loss. Through adding new revenue streams, netTALK aims to reverse this trend.

NetTALK’s entrance into the data center space marks another move in its strategy to diversify its revenue streams. The CLEC recently inked a multi-year deal with wireless wholesaler LightSquared to gain access to its 4G-LTE network. NetTALK plans to brand and sell its own wireless voice and data packages to complement its wireline VoIP offerings.

In the Miami data center, newly named the netTALK Cloud Center, netTALK acquires a property currently occupied by major players in telecom—Sprint Nextel Corp, Fibernet, Qwest/CenturyLink, AT&T Wireless and Verizon Wireless among others. In addition to operating the data center and providing cloud hosting and other managed services, netTALK will also use the property to provide connectivity for its wireless customers, courtesy of the data center's 4G enabled cell tower.

"Building on our recently-announced multi-year wholesale agreement with LightSquared, this facility provides us with additional capacity, power efficiencies and equipment such as a high-bandwidth antennae, which are key to our strategic growth plans, current and future, including television and wireless 4G transmissions,” commented netTALK President Anastasios Kyriakides.

NetTALK is attempting to replicate in wireless what it already offers through wireline—low cost phone service to customers anywhere in the United States and Canada. In the next year, it will add wireless voice and mobile broadband to its arsenal of services thanks to its LightSquared agreement and cell tower purchase. According to Kyriakides, the company is also developing a television product—netTALK TV—that will round out its triple play offering.

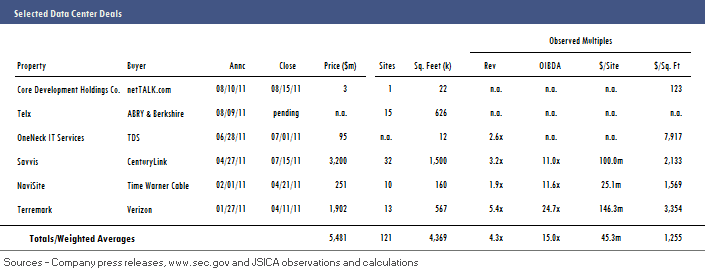

NetTALK’s $2.7m acquisition is the most recent purchase in an active data center market. Telx, a leading data center operator, announced in early August that it agreed to be purchased by two private equity firms in Boston, while telcos TDS and Centurylink finalized their acquisitions of OneNeck IT Services and Savvis in July. NetTALK recently confirmed to JSI Capital Advisors that it plans to expand its data center footprint in the future.

The opportunity for growth in data centers explains why many buyers are surfacing. According to Tier1 Research, revenue generated by data center operators will reach $8.1b in 2011, up from $5.7b in 2009—a 42% increase over two years. For netTALK, its data center purchase could prove even more beneficial, providing it not only with revenues from network operations and cloud hosting, but with wireless revenues as well.

Adam Brissette

Adam Brissette