But is “Growth by Acquisition” Really Growth?

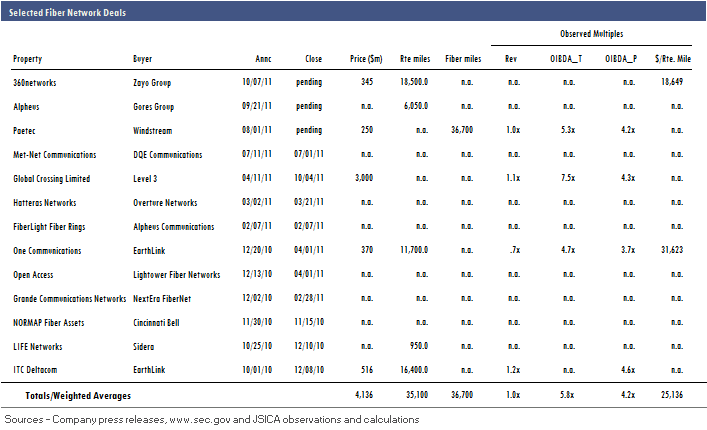

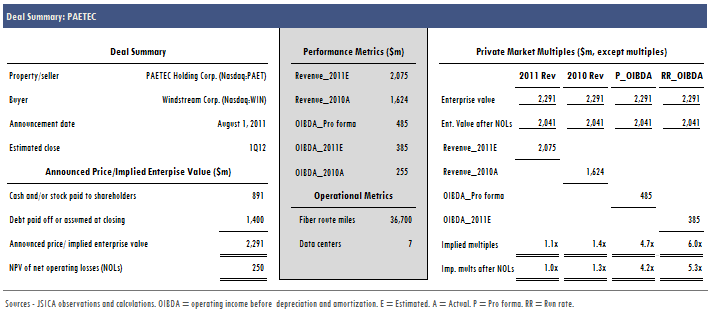

Jeff Gardner and the team at Windstream (Nasdaq:WIN) sure don’t like to let their seats at the deal table grow cold…Monday the company announced its ninth acquisition since the company was formed in a spin/reverse merger between the former Alltel wireline operations and Valor Communications, in mid-2006. The $2.3b deal for CLEC/fiber network/managed services provider PAETEC (Nasdaq:PAET) is Windstream’s largest to date; when Alltel Wireline merged with Valor, Valor was valued at just more than $2b. Since then numerous sub-$1b buys have been completed (more on that below).

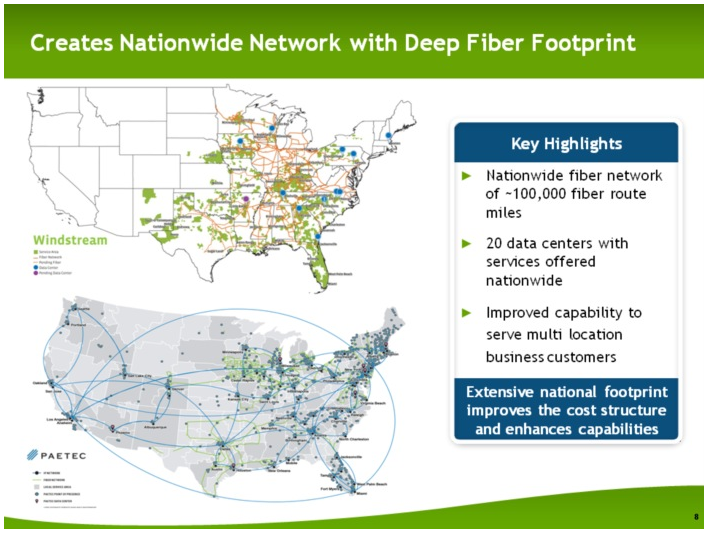

The deal has all of the criteria that Gardner et al have touted in many of the deals announced since 2009: it will increase the company’s reliance upon business and broadband services—to 70% pro forma PAETEC. In a press release, Gardner said, "This transaction significantly advances our strategy to drive top-line revenue growth by expanding our focus on business and broadband services. The combined company will have a nationwide network with a deep fiber footprint to offer enhanced capabilities in strategic growth areas, including IP-based services, data centers, cloud computing and managed services. Financially, we improve our growth profile and lower the payout ratio on our strong dividend, offering investors a unique combination of growth and yield."

Under the terms of the deal, PAETEC shareholders will receive 0.460 shares of Windstream common stock for each PAETEC share owned. Windstream expects to issue approximately 73m shares of stock valued at approximately $891m, based on its closing stock price on July 29, 2011. Windstream also will assume or refinance PAETEC's net debt of approximately $1.4b. PAETEC stockholders are expected to own approximately 13% of the combined company at close, and the deal has been approved by the boards of directors of both companies.

As in most of the deals Windstream has done, management anticipates significant synergies--$100m in operating expenses three years out and another $10m in capital expense savings. Additionally, PAETEC has significant Net Operating Losses that will provide Windstream with a tax shield; the company pegs the net present value of those NOLs at $250m. The company expects to incur about $50m in operating and integration costs in the first year after close and will invest $55m in capex over the first three years of ownership. The deal is expected to close in the first quarter of 2012. Windstream also said that the buy will slightly delever its balance sheet, after synergies, and reiterated its goal of reducing debt to cash flow to 3.2x-3.4x. The company has received $1.1b in financing commitments for the deal and noted that its present dividend of $1/year will be maintained.

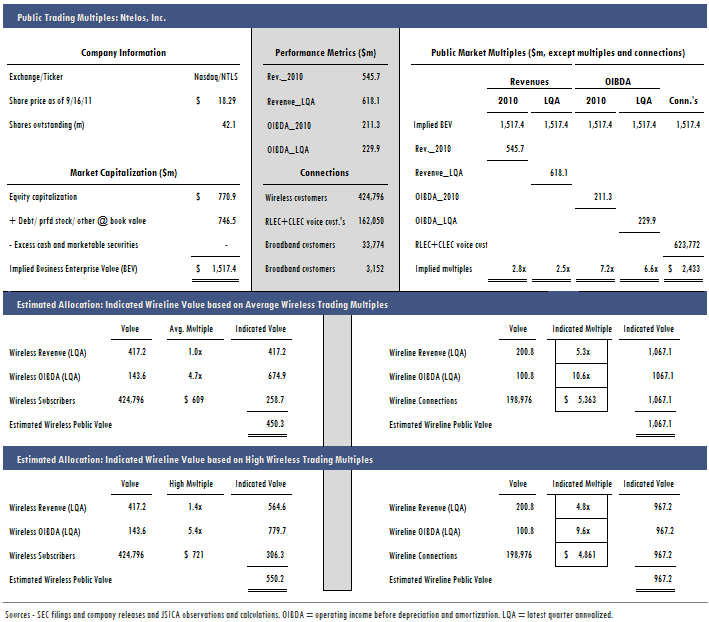

Running the numbers through the calculator shows the revenue multiple on the deal to be just over 1x run-rate revenue, while the run-rate cash flow multiple is about 6x. Pro forma the synergies and adjusting for the NPV of the NOLs pushes that cash flow multiple down to about 4.2x.

In its conference call discussing the deal, Gardner pointed out the strong growth profile of the areas where it/PAETEC see their upside: Wireless backhaul is expected to grow 32%, Ethernet services, 31%; MPLS, 14% and Hosting Services, 9%.

And in the press release, PAETEC ceo Arunas Chesonis said, “Both PAETEC and Windstream are built on a customer and employee-focused culture. Together, with far denser network assets, an expansive fiber infrastructure, and larger data center footprint, I believe our brightest days are ahead. Our combination now creates a new Fortune 500 company with the financial strength and scale to compete and win against any other provider in the industry.”

That sounds great guys, and Windstream’s transition from a consumer-centric business to one focused on enterprise and broadband services is clearly occurring. But what about growth?

I decided to take a look at all of Windstream’s deals since the company’s inception and analyze the actual growth in revenue. Admittedly, an analysis of cash flow might better demonstrate the “value” of these deals, but for simplicity sake let’s look just at the top line.

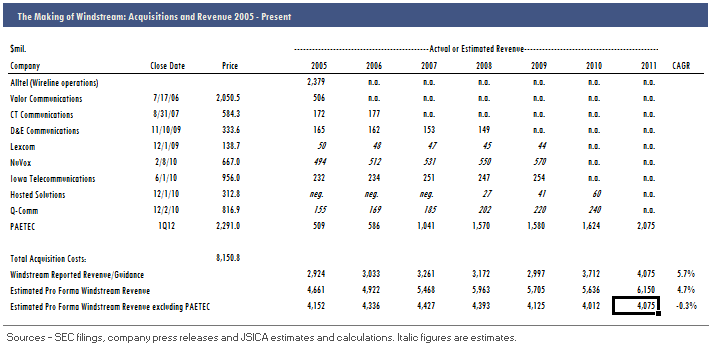

First of all, in all fairness, the “business and broadband” growth strategy didn’t clearly emerge until sometime in 2009. Prior to that, Windstream’s deals were focused on buying scope and scale, pure and simple. It acquired CT Communications in mid-2007 and also acquired D&E Communications, Lexcom and Iowa Telecom over the next few years. These telcos probably didn’t offer that much in the way of “B&BB” growth profiles, but synergies and scale should make for improved cash flow. Meanwhile, the NuVox, Hosted Solutions, Q-Comm and PAETEC deals, announced or closed over the past year and a half, all played into the Windstream “B&BB” strategy.

So, I built a chart showing the historic revenue of all of the piece parts that now comprise Windstream. Several of the companies acquired by Windstream were public, and for the four that weren’t I’ve done estimates based on data provided with deal announcements and closing announcements. These estimates may not be perfect, but the trend that we see overall is, in my view, verifiable: Windstream’s acquisitions have not actually led to measurable growth in the top line on a pro forma basis. In fact, if you back out PAETEC's very high, also acquisition-fueled growth, the compound annual growth rate for Windstream pro forma is -0.3%.

As it turns out, Windstream has experienced flat to down results for each of the years since it was formed. The following quotes are taken verbatim from Windstream’s earnings releases for 1Q11 as well as the full years 2007 - 2010:

As it turns out, Windstream has experienced flat to down results for each of the years since it was formed. The following quotes are taken verbatim from Windstream’s earnings releases for 1Q11 as well as the full years 2007 - 2010:

1Q11: Under pro forma results:

- Revenues were $1.023 billion, a 1.8 percent decrease from a year ago.

- Operating income before depreciation and amortization (OIBDA) was $496.7 million, essentially unchanged year-over-year.

2010: Under pro forma results, which include results for NuVox Inc.; Iowa Telecommunications Services, Inc.; Hosted Solutions Acquisition, LLC, and Q-Comm Corporation for the entire year:

- Revenues were $4.1 billion, a 2 percent decrease from a year ago.

- OIBDA was $1.98 billion, a 2 percent increase year-over-year.

2009: Under pro forma results from current businesses, which include D&E and Lexcom results for the entire year:

- Revenues were $3.121 billion, a 5 percent decrease from a year ago.

- OIBDA was $1.591 billion, an 8 percent decrease year-over-year.

2008: Under pro forma results from current businesses:

- Revenues were $3.172 billion, a 1.5 percent decrease from a year ago.

- Operating income before depreciation and amortization was $1.638 billion, a 1 percent decrease year-over-year and includes $8.5 million in restructuring charges.

2007: Among the pro forma highlights for 2007 from current businesses:

- Revenues were $3.262 billion, a 1 percent increase from a year ago.

- Operating income before depreciation and amortization was $1.657 billion, a 1 percent increase year-over-year.

Now, have a look at this line from PAETEC’s first quarter 2011 report:

Actual First Quarter 2011 compared to Pro Forma First Quarter 2010

The following pro forma results for first quarter 2010 give effect to PAETEC’s acquisition of Cavalier Telephone as if it had occurred at the beginning of 2010…Actual total revenue of $495.5 million for first quarter 2011 represented an increase of 2.5% or $12.3 million over pro forma total revenue of $483.2 million for first quarter 2010. The increase in actual total revenue was primarily attributable to increased revenue from PAETEC’s acquisition of Quagga in June 2010 and U.S. Energy in February 2010.

Sooo…Pro forma PAETEC’s own recent acquisition of Cavalier Telephone, growth in the first quarter was 2.5%--but that is attributable to PAETEC’s buys of Quagga and U.S. Energy…I don’t have the breakouts, but it sounds to me like PAETEC’s actual pro forma revenue trend was negative, or flat at best.

What’s my point? Deals can be packaged to demonstrate “growth” prospects—and I do think the whole “cloud/data centers/managed services” realm offers a brighter outlook for telephone companies than say, improving DSL penetration. But the real “growth” that these deals appear to deliver is coming from cost cutting and efficiencies created when two organizations combine (i.e. people get fired). And once you’ve cut as much as you can cut, that ice cube is still melting…Even more disconcerting? The pro forma cash flow figures reported above are mostly negative.

Adam Brissette

Adam Brissette