CNSL Acquires 146k Commercial and Business Subs

Matoon, Illinois-based Consolidated Communications announced on February 6 that it had entered into an agreement to acquire Roseville, California-based SureWest Communications. Under the terms of the deal, Consolidated will acquire all outstanding shares of the publicly-traded SureWest at a price of $23 per share, translating into an overall price of $340.9m. The deal marks Consolidated’s first major acquisition since acquiring North Pittsburgh Systems in 2007 and breathes some life into what has been a slow M&A scene for ILECs.

Rumors of SureWest as a potential acquisition target had trickled out over the past few weeks, but Consolidated was never linked as the potential buyer. Google was rumored to have an interest in the company as the technology giant works to build its 1Gbps fiber network in Kansas City. Because of SureWest’s ongoing FTTH build in nearby Olathe, Kansas, and its fiber network that reaches 94k homes in and around Kansas City, the company could have been used to help Google establish its model network.

On Monday however, it was Consolidated that emerged as a buyer for SureWest, in a deal that significantly expands Consolidated's operations. Consolidated adds SureWest’s 130k residential subscribers and 16k business customers in the greater Sacramento and Kansas City regions, which account for approximately 343k voice, video, and Internet connections. Through the transaction, Consolidated will nearly double its broadband subscribers as SureWest in recent years has shifted its service mix more heavily towards broadband. In fact during 3Q11, SureWest generated 76% of its revenues from its broadband segment. Pro forma SureWest, business and broadband services will generate over 70% of Consolidated's revenue.

The combined company, on a pro forma basis, would have generated approximately $620m in revenue and $229m in cash flow for the trailing twelve months (TTM) ended September 30th. Consolidated's management projects annual operating synergies of $25m with the deal and another $5m-$10m of capital expenditure synergies. In addition to the anticipated cost savings, the deal benefits Consolidated from a tax perspective as well, given SureWest's NOLs of approximately $67m.

The acquisition is expected to be accretive on a cash flow basis in the first year post-close for Consolidated, assuming cost targets are met. Pro forma the SureWest acquisition, Consolidated's cash flow margins for the TTM ended September 30th actually decline to 37% from 40% due to SureWest's relatively low 32% OIBDA margins. While the company expects its anticipated synergies to be fully realized in the first full year after the transaction’s close, the savings will be offset in the short-term by merger and integration costs, projected at $20m and $25m for the first two years post-close.

Turning to the balance sheet, Consolidated management noted that the transaction was deleveraging for the company. Consolidated currently finances its operations primarily with debt, carrying a debt to equity ratio of approximately 1.5. By contrast, SureWest’s capital structure the day before announcement was approximately 48% debt and 52% equity, or a 0.6 debt to equity ratio.

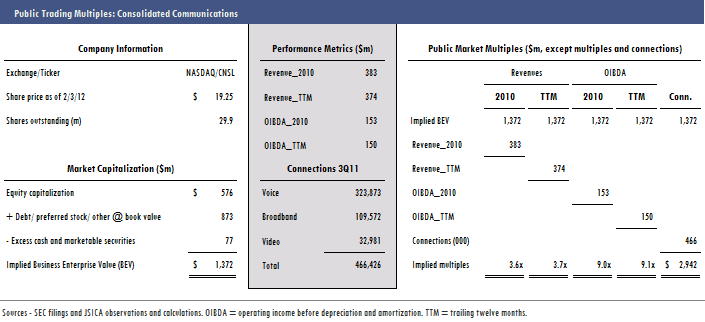

At the announced price of $23 per share, Consolidated agreed to pay a premium of 47% over SureWest’s recent closing price of $15.59. Consolidated's management reported deal multiples of 2.2x trailing revenue and 6.3x adjusted trailing OIBDA. After factoring in the transaction’s anticipated $25m in annual operating cost benefits, the cash flow multiple drops to 4.8x, or about $1,548 per connection. Consolidated didn't disclose its valuation of SureWest's NOLs, but based on the reported multiples it appears that the NOLs were valued at a relatively conservative $8m.

Should the public continue to trade shares of Consolidated near its recently observed public trading multiples, the company's stock price stands to benefit from the deal. The market is currently trading shares of Consolidated at multiples well above the prices it paid for SureWest. Based on recent levels, investors are trading Consolidated at 3.7x trailing revenue and at 9.1x trailing OIBDA compared to the SureWest's price tags of 2.2x revenue and 6.3x cash flow.

In recent quarters, Consolidated has struggled to generate growth and its management has watched the company's top line slip 3% year over year. Acquiring SureWest is an aggressive move to reverse this downward trend.

While Consolidated spent 2011 focusing on cost cutting efforts to maintain profitability, SureWest invested in growth initiatives, spending $64m, or 25% of revenues, to expand its fiber network and to increase wireless backhaul capacity. Looking back even further to the years 2008-2010, SureWest has consistently spent over 20% of its top line on fiber related investments. The company invested a high of $86.5m during 2008, a year in which SureWest closed on its $173m acquisition of Everest Broadband, establishing its fiber footprint in Kansas City. With SureWest positioned for future growth in its broadband services, the deal’s forward looking multiples appear favorable for Consolidated.

Deal Advisor,

Deal Advisor,