Thursday

Jun182015

QTS Realty Acquires Carpathia Hosting

QTS Realty Trust, Inc. (NYSE: QTS) announced on Wednesday, June 17th that it had closed its acquisition of Carpathia Hosting, Inc. for approximately $326.0 million. The deal was originally announced on Wednesday, May 6th. The acquisition significantly increases QTS’ data center footprint and grants access into new domestic and international markets.

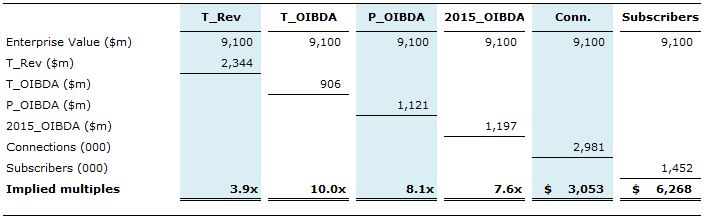

Valuation Analysis and Deal Metrics

Transaction Facts

- QTS Realty is an industry-leading provider of hybrid cloud services and managed hosting.

- Carpathia Hosting is an industry-leading provider of colocation, cloud and managed services.

- Acquisition will be financed through approximately $290.0 million in cash and $36.0 million in capital leases that are expected to be funded on a leverage neutral basis.

- Carpathia Hosting has approximately 8 domestic and 5 international data centers.

- Carpathia’s portfolio of data centers equals approximately 66,700 square feet in total.

Strategic Considerations

- QTS Realty gains approximately 230 commercial and federal customers as a result of the acquisition.

- Increases QTS’ average MRR per customer from $15,000 to $27,000.

- $2.0 million in expected synergies for QTS are expected in 2016 as a result of the transaction.

- Carpathia’s footprint in North America is complementary to support QTS’ Federal Government business.

- Transaction provides QTS with entry into markets such as Toronto, Amsterdam, London, Hong Kong, and Sydney.

JSICA’s Take

- Acquisition of Carpathia Hosting will allow QTS Realty to add an international presence, as well as diversify its footprint across North America.

- QTS Realty will be able to differentiate itself in industry channels such as Healthcare and Government, which are highly regulated.

tagged  Carpathia Hosting, QTS Realty in Deal Advisor, Deals: Data Center

Carpathia Hosting, QTS Realty in Deal Advisor, Deals: Data Center

Deal Advisor, Deals: Data Center